Learn how an LLC can help protect personal assets, separate finances, and create a stronger foundation. Know 13 reasons why you should start an LLC today!

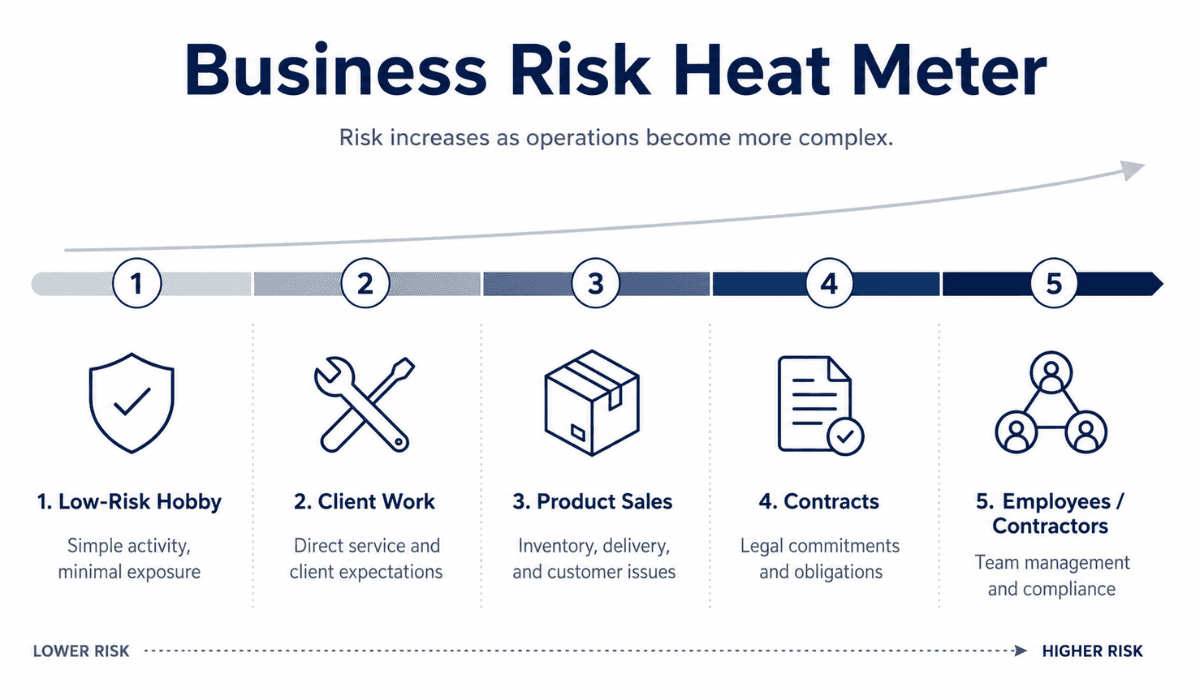

You started your business from home because it was simple and low-cost. A few months in, and things look different. You have employees, you are signing contracts, and orders are getting bigger. Your income has grown, and so has your risk.

That is usually when the questions start.

- Should I form an LLC or stay a sole proprietor?

- Does my current structure offer limited liability?

- What are the benefits of forming an LLC over a sole proprietorship?

Forming an LLC is not just paperwork. It changes how your business is taxed, how clients and lenders see you, and whether you can bring in investors down the line. The clearest way to answer these questions is to understand why other sole proprietors make the switch.

Sole Proprietorship vs. LLC: What Changes

A sole proprietorship is often the default setup for a one-person business. If you start doing business by yourself and do not form another business entity, you may be operating as a sole proprietor.

An LLC is different. It is a business entity created under state law. A single owner can form a single-member LLC. As per the U.S. Small Business Administration, an LLC combines the liability protection of a Corporation with the tax flexibility of a partnership [1].

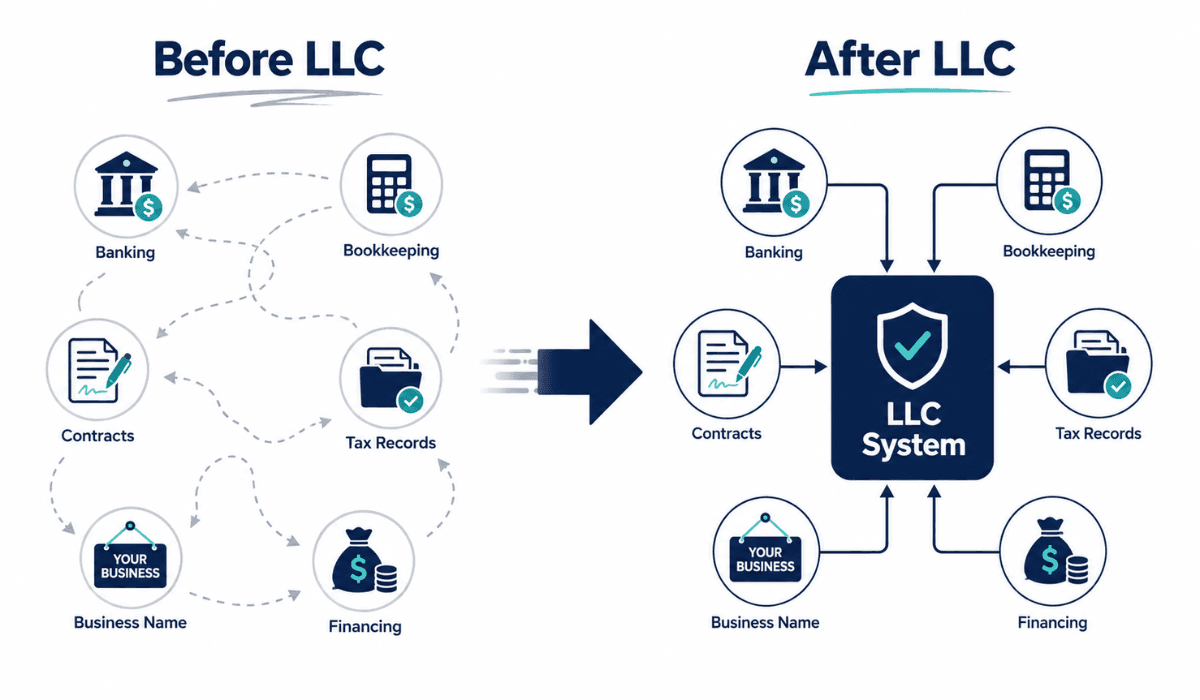

The biggest change is structure. A sole proprietorship keeps the owner and the business closely connected. An LLC creates legal separation between the two.

Here is a simple comparison:

Factor | Sole Proprietorship | LLC |

Formation | Simple to start | Requires state filing |

Legal structure | Owner and business are closely linked | Business can be separate from the owner |

Liability | Owner may be personally responsible | May help protect personal assets |

Taxes | Reported on the owner’s personal return | Usually pass-through by default |

Credibility | Less formal | More formal business identity |

Banking | Can be less structured | Easier to separate accounts |

Growth | Simple but limited | Better structure for growth |

For a deeper comparison, read our guide to sole proprietorship vs. single-member LLC.

13 Reasons Sole Proprietors Should Consider Forming an LLC

1. To Help Protect Personal Assets

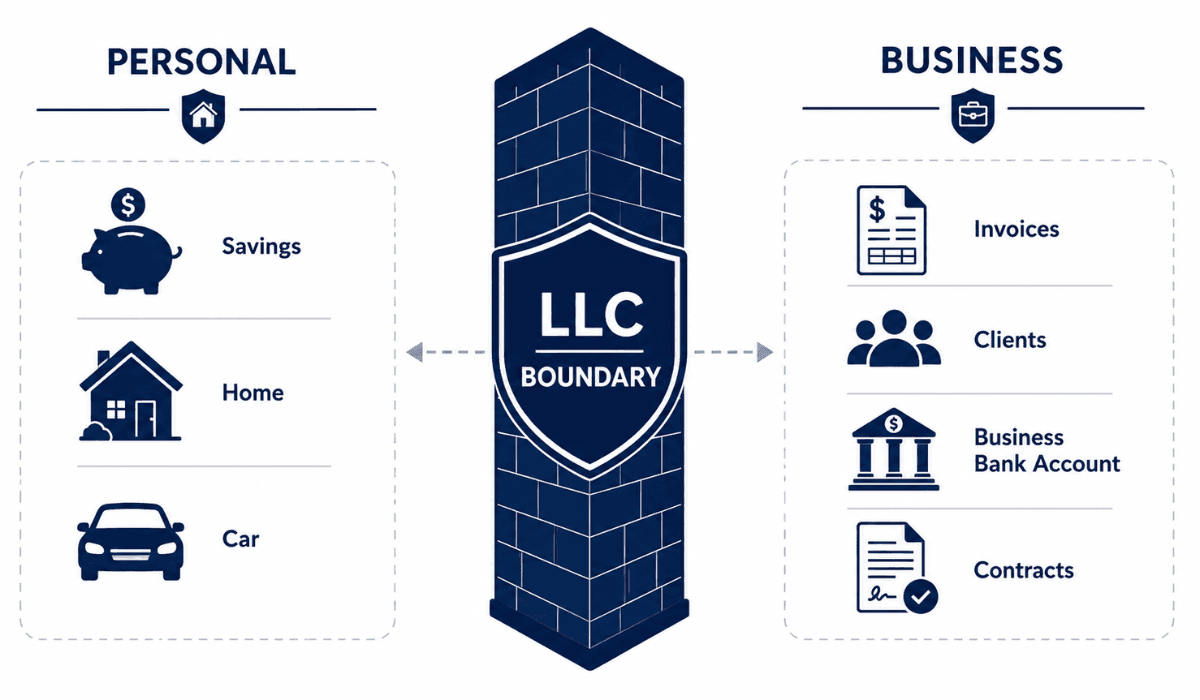

One of the benefits LLCs offer that sole proprietors don’t is liability protection. As a sole proprietor, your personal and business finances are the same thing. If your business takes on debt, faces a lawsuit, or cannot pay a vendor, your personal assets, including your savings, your car, and potentially your home, can be at risk.

Forming an LLC creates a legal boundary between you and the business. The SBA confirms that LLCs protect you from personal liability in most instances, so your personal assets won't be at risk if your LLC faces bankruptcy or lawsuits. This matters most if your work involves client property, equipment, contracts, or anything that carries operational risk.

Note: This protection has limits. If you mix personal and business finances, or don't maintain the LLC properly, courts can still hold you personally liable. But for a growing sole proprietorship, an LLC remains one of the most direct ways to separate business risk from personal life.

2. To Create Legal Separation Between You and the Business

A sole proprietorship does not give your business its own legal identity; you and the business are the same entity in the eyes of the law. An LLC changes that. You begin operating through a registered company rather than only as an individual.

This shift becomes more useful as your business accumulates a name, client agreements, recurring payments, software subscriptions, and inventory. An LLC gives you one structure to organize all of it under, and it gives banks, vendors, and partners a clearer picture of who they are doing business with.

3. To Look More Professional to Clients and Customers

Many sole proprietors start by using their personal name, which works fine early on. As the business grows, a formal LLC name appearing on invoices, contracts, proposals, business bank accounts, and vendor forms signals that clients are working with an established business rather than an informal side project.

An LLC will not replace good service or strong communication. Those still matter most. But credibility on paper supports credibility in practice, and that combination is part of why LLC adoption has accelerated industry-wide.

4. To Separate Personal and Business Finances

Many sole proprietors mix personal and business money without meaning to. Client payments land in a personal checking account. Business tools get charged to a personal card. Over time, this makes it difficult to see what the business actually earns, spends, or keeps as profit.

Forming an LLC gives you a clear reason to open a separate business bank account. It can also help you use separate payment processors, business cards, and bookkeeping tools. This also makes it easier to see:

- What the business earns

- What the business spends

- Which expenses belong to the business

- How much profit is left

- What records do you need for tax time

5. To Organize for Tax Time, Not to Lower Taxes

This is the most misunderstood reason on this list, so it is worth stating clearly. Forming an LLC does not automatically lower your taxes. According to the IRS, a single-member LLC ( not elected to be treated as a corporation) is a disregarded entity, and its activity is reported on the owner's personal tax return, typically using Schedule C [2].

In other words, the IRS taxes a default single-member LLC almost the same way it taxes a sole proprietorship. What changes is the organization, not the tax rates. With separate business records, it becomes far easier to track income, expenses, and deductions, and to hand clean numbers to a tax professional instead of sorting through a single mixed account.

6. To Unlock Flexible Tax Options as You Grow

While the default tax treatment is similar to a sole proprietorship, an LLC is not locked into it. Per the IRS, an LLC can file Form 8832 to elect corporate tax treatment instead of being treated as a disregarded entity [3], and many growing LLCs eventually file Form 2553 to elect S corporation status once profits are steady enough to justify it.

This is not the right move for every business, and an S corp election adds its own payroll and compliance requirements. But the option does not exist for a sole proprietorship. The real benefit of an LLC here is optionality: you can start simple and elect a different tax structure later if your income and goals support it.

7. To Sign Contracts Under a Business Name

As your business grows, you will likely sign client agreements, vendor contracts, leases, or retainers more often. As a sole proprietor, you typically sign those documents under your personal name. An LLC lets you sign under the business name instead, which keeps your identity consistent across every agreement and makes it clear to clients exactly who they are contracting with.

8. To Build Business Credit

A sole proprietor typically relies on personal credit to cover business needs, from a credit card to equipment financing. An LLC gives you a formal business identity that lenders and vendors can extend credit to directly, which supports a cleaner path toward a business credit card, vendor terms, a business line of credit, or equipment financing.

Lenders may still review your personal credit and financial history, especially for a new or small business, and an LLC does not guarantee approval. But it is a necessary step toward eventually separating your business credit profile from your own.

9. To Hire and Subcontract With Less Risk

Bringing on your first employee or contractor adds real responsibility: payment records, insurance requirements, and clear business policies. Operating that relationship through an LLC, rather than as an individual, gives you a more defined structure for managing those obligations and tends to make the business look more established to the people you bring on. If you are planning to hire even one contractor, this is usually the point where a sole proprietorship starts to feel insufficient.

10. To Move at the Same Pace as the Broader Market

This reason is less about your business specifically and more about timing. Roughly 4.1 million new LLCs were formed in the U.S. in 2025, and the structure now accounts for the large majority of new business formations nationwide. [4]

That shift reflects a broader recognition among small business owners that liability protection and tax flexibility are worth the modest cost and paperwork of forming an LLC, especially compared to the unlimited personal exposure of a sole proprietorship.

11. To Protect and Formalize the Business Name

Many sole proprietors start under their personal name. Others use a DBA, which stands for “doing business as.” A DBA can let you use a business name, but it does not create the same legal structure as an LLC.

When you form an LLC, you register the business name with the state. This can help protect that name at the state level and make the business identity more formal.

Your business name can appear on your website, invoices, contracts, social media, product packaging, and local listings. If that name matters to your growth, forming an LLC may be a good next step.

Note: Keep in mind that an LLC name is not the same as a trademark. A trademark can provide broader brand protection. But forming an LLC can still help you secure your business name in your state.

For more on business names, read our guide to DBA vs LLC.

12. To Create a Better Structure for Growth

A sole proprietorship works well at a small scale, but it has a ceiling. Growth, whether through more clients, new markets, additional partners, or eventually selling the business, requires a foundation that can hold that weight. An LLC gives you a defined structure for how the business operates and how decisions get made, and an operating agreement can spell out ownership and management roles if you bring on additional members later.

13. To Treat the Business Like a Long-Term Company

At some point, the way you manage the business needs to align with how it is actually growing. Forming an LLC supports that shift: separated finances, organized records, a registered name, and a structure built for continuity rather than a single person's side project. That mindset tends to produce better decisions on pricing, spending, and planning.

An LLC by itself is not proof that a business is serious. But for most growing sole proprietors, it is one of the clearest, most practical steps toward building something durable.

Also read: Should I Start an LLC Today or Wait? A Decision Guide for Startups

When an LLC May Not Be the Right Next Step Yet

An LLC is not the right move for every sole proprietor at every stage.

You may want to wait if your business is still more of a hobby than a business, with little income, low risk, and no clear plan to grow. You may also want to wait if the ongoing costs, including state filing fees, annual reports, registered agent fees, and franchise taxes in some states, do not fit your current stage.

Recordkeeping matters too. An LLC works best when you actually keep business and personal finances separate. If you are not ready to open a dedicated account and track records consistently, it may be worth building those habits first.

Some businesses need a different structure entirely. A startup planning to raise venture capital, for example, may want to compare an LLC against a C corporation rather than defaulting to an LLC.

The goal is not to form an LLC because other business owners are doing it. The goal is to opt for the structure that fits your business now and supports where you want to go next.

Also Read: What is a C Corporation? The complete guide for business owners (2026)

How to Change From Sole Proprietor to LLC

To convert, you generally form a new LLC with your state and begin operating the business under that entity. The typical steps include:

- Choosing a business name

- Filing formation documents with the state

- Appointing a registered agent

- Creating internal company records

- Getting an EIN if needed

- Opening a business bank account

- Updating contracts, invoices, payment accounts, and licenses to the new LLC name

Exact requirements vary by state and business type. For a full walkthrough, read our how to form an LLC guide!

Final Takeaway

If your business now has regular income, contracts, expenses, or growth goals, forming an LLC may be a practical next step. If you are ready to move from sole proprietor to LLC, Swyft Filings can help you form your LLC and take the next step with confidence.

Bibliography

- U.S. Small Business Administration. Choose a Business Structure. Accessed June 19, 2026.

- Internal Revenue Service. Single Member Limited Liability Companies. Accessed June 19, 2026.

- Internal Revenue Service. LLC Filing as a Corporation or Partnership. Accessed June 19, 2026.

- Small Biz Statistics. How Many LLCs Are Formed Each Year in the United States? Accessed June 19, 2026.