You have built a business that is actually making money. Now every dollar of profit gets hit with a 15.3% self-employment tax before you see a cent of it. But there is a way to change that.

An S corporation is a federal tax election that changes how the IRS taxes your business income. Unlike what many people mistakenly believe, it does not replace your LLC or corporation; it sits on top of it. And for the right business at the right income level, it can shift thousands of dollars from the IRS back into your pocket each year.

This guide covers how S corp taxation actually works in 2026, what the IRS requires from you, how to know if the savings are real for your situation, and exactly what filing the election involves.

Why S Corp Status Matters More in 2026?

2026 is not the same landscape for business taxation as it was three years ago.

The One Big Beautiful Bill Act (OBBBA) made the 20% Qualified Business Income (QBI) deduction under Section 199A permanent. That is a meaningful shift. It means S corp owners who were holding off now have a more stable foundation to plan around.

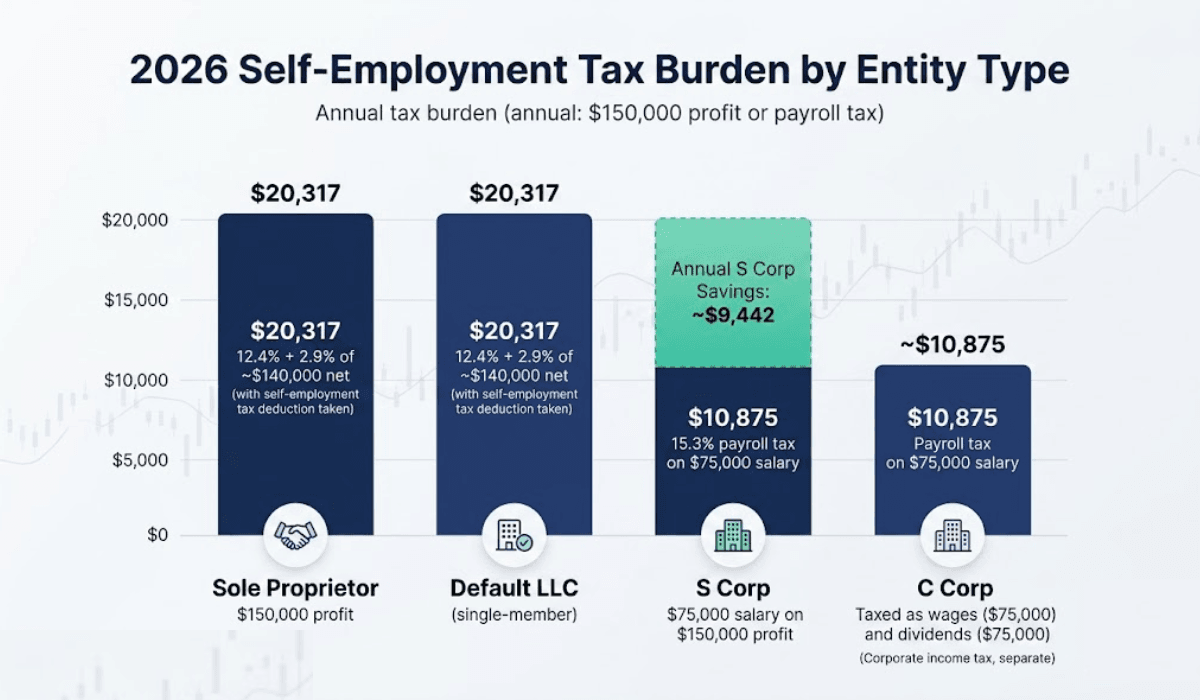

At the same time, self-employment tax rates have not changed. A sole proprietor or default LLC owner still pays 15.3% on every dollar of net profit up to $176,100, then 2.9% on everything above that. For a business making $150,000 in net profit, that is $22,950 in self-employment taxes alone, before a single dollar of income tax.

An S corp election does not eliminate that bill. But it changes the math significantly.

How S Corp Taxation Actually Works?

The Pass-Through Structure

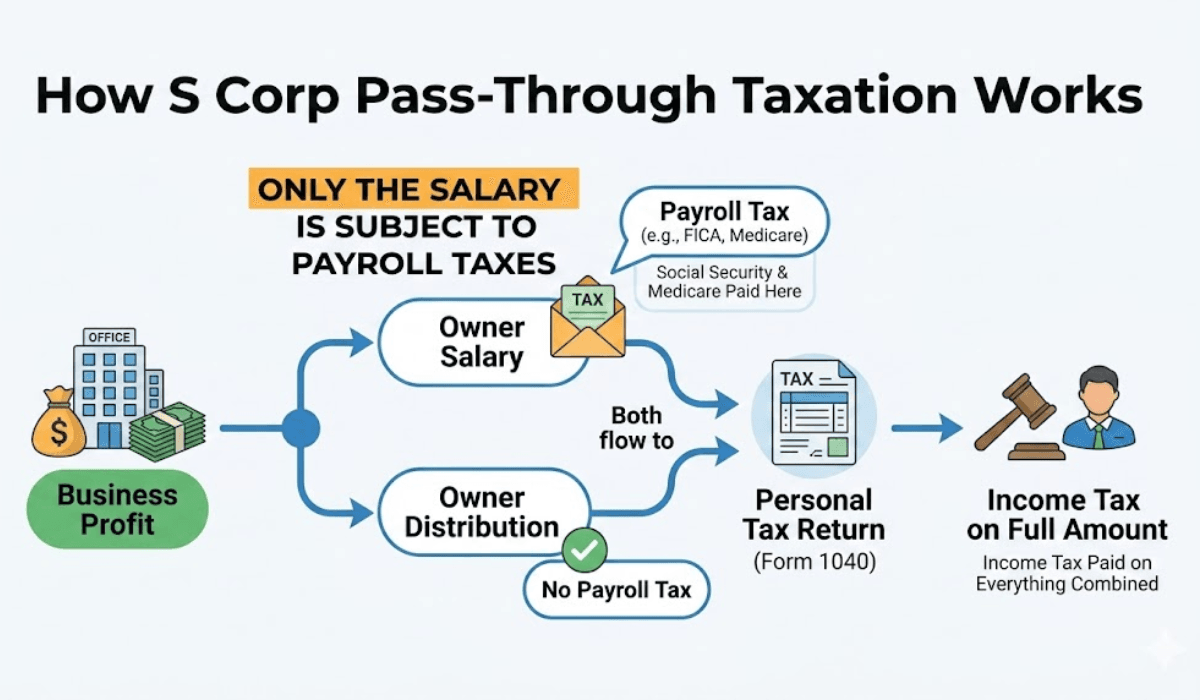

An S corp does not pay federal income tax at the business level. The IRS classifies S Corps as pass-through entities, meaning all profits, losses, deductions, and credits flow directly to the shareholders' personal tax returns. [1]

This is different from a C corp, which pays corporate tax first. With an S corp, the business files an informational return using Form 1120-S, and each shareholder receives a Schedule K-1 showing their portion of income and deductions. [2]

The Salary-Distribution Split: Where the Savings Live

Here is where S corp taxation becomes a strategy, not just a label.

As an S Corp owner who works in the business, the IRS requires you to pay yourself a reasonable salary. That salary goes through payroll. It is subject to Social Security and Medicare taxes, just like any employee's wages.

But any profit above that salary can be taken as an owner's distribution. Distributions are not subject to self-employment tax.

Type | Default LLC | S Corp |

Net Profit | $150,000 | $150,000 |

Reasonable Salary | N/A | $75,000 |

Owner Distribution | N/A | $75,000 |

Self-Employment / Payroll Tax Base | $150,000 | $75,000 |

SE / Payroll Tax (15.3%) | $22,950 | $11,475 |

Annual Tax Savings | — | ~$11,475 |

After payroll service costs and tax prep fees (typically $3,500–$5,000 per year), the net savings in this scenario land around $6,500–$8,000. That is real money that stays in your business.

How the QBI Deduction Stacks On Top

S corp owners may also qualify for the Section 199A Qualified Business Income deduction, which allows eligible owners to deduct up to 20% of qualified business income. Now that this deduction is permanent under the OBBBA, it provides an additional layer of tax relief on top of the payroll tax savings. [3]

Not every business qualifies. Specified Service Trades or Businesses (SSTBs), like law firms or financial advisors, face phase-out limits at higher income levels. A tax professional can confirm whether your business qualifies and at what threshold.

Not every business qualifies. Specified Service Trades or Businesses (SSTBs), like law firms or financial advisors, face phase-out limits at higher income levels. A tax professional can confirm whether your business qualifies and at what threshold.

The Reasonable Salary Rule: What the IRS Expects

The IRS does not allow S corp owners to take zero salary and receive all income as distributions. If that were allowed, every business owner would skip payroll taxes entirely.

To prevent that, the IRS requires S corp owner-employees to pay themselves a salary that reflects what the market would pay someone to do the same work. This is called the reasonable salary requirement.

How to Determine a Reasonable Salary

There is no exact formula. But the IRS evaluates salaries based on several factors:

- Your role and the hours you work in the business

- What similar positions pay in your industry and region

- The profitability of the business

- Your training, experience, and qualifications

Practical reference points include Bureau of Labor Statistics wage data, industry compensation surveys, and what the business would need to pay a hired replacement. [4]

A common approach many CPAs use: pay yourself what a qualified employee in your role would reasonably earn, then take the remaining profits as distributions. If your business generates $200,000 in profit and your role would command $90,000 on the open market, a $90,000 salary is a defensible starting point.

What Happens If Your Salary Is Too Low

If the IRS audits your return and finds your salary unreasonably low, it can reclassify distributions as wages. That triggers back payroll taxes, plus interest and penalties on the reclassified amount.

This is one of the main reasons S Corps receive closer IRS scrutiny than standard LLCs. Good documentation matters. Keep records that support why your salary is reasonable: job descriptions, industry data, and how you calculated the number.

S Corp vs. LLC vs. C Corp: A Side-by-Side Tax Breakdown

Understanding the differences between these three structures is central to making the right call for your business.

S Corp vs. C Corp: Double Taxation vs. Pass-Through

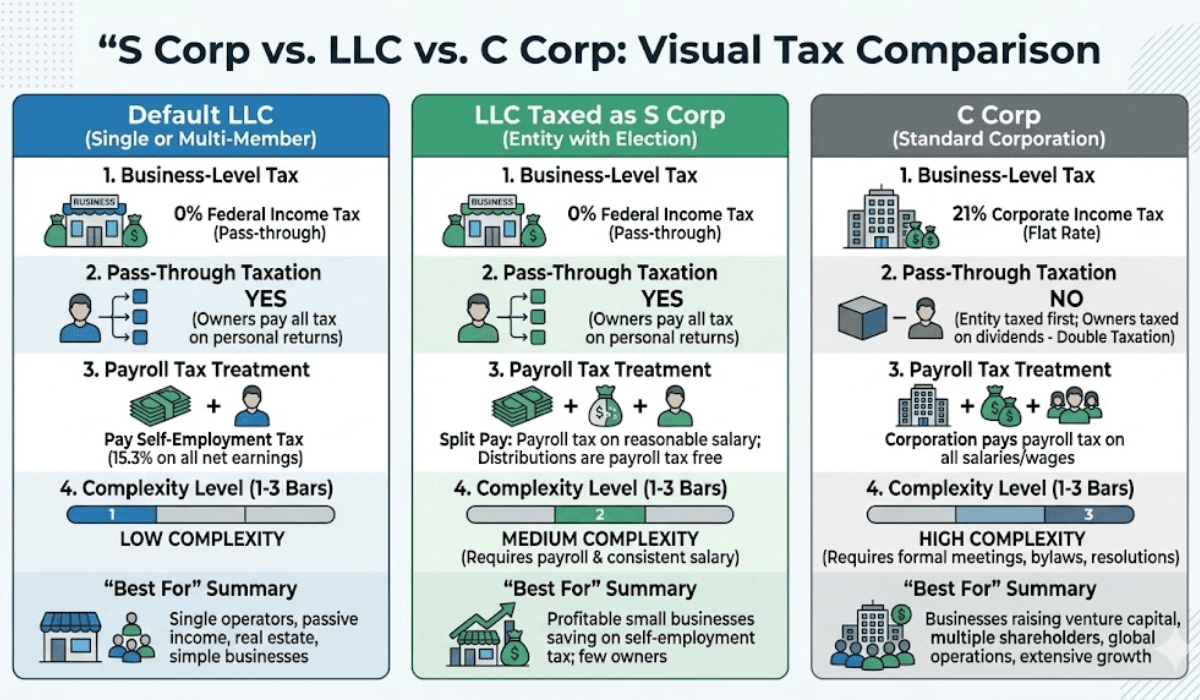

A C Corp pays federal income tax at the 21% corporate rate on its profits. Then, if those profits are distributed to shareholders as dividends, shareholders pay personal income tax on those dividends again. That is the double taxation most business owners want to avoid.

An S corp skips the first layer entirely. Profits flow directly to shareholders, who pay personal income tax once at their individual rate.

The catch: S corps have structural limits that C corps do not. A maximum of 100 shareholders, one class of stock, and no foreign shareholders. C corps have none of these restrictions, which is why venture-backed and publicly traded companies use them.

S Corp vs. LLC: Same Pass-Through, Different Tax Base

Both structures offer pass-through taxation. Both offer liability protection. The difference is in what gets taxed.

A default LLC owner pays self-employment tax (15.3%) on all net profit. An LLC that has elected S corp status pays payroll taxes only on the owner's salary, not the total profit.

Feature | Default LLC | LLC Taxed as S Corp | C Corp |

Federal income tax at the entity level | No | No | Yes (21%) |

Pass-through to personal return | Yes | Yes | No (dividends only) |

SE/payroll tax on all profits | Yes | No (salary only) | N/A |

Payroll required | No | Yes | Yes |

Shareholder limit | None | 100 max | Unlimited |

Foreign shareholders allowed | Yes | No | Yes |

Annual federal filing | Schedule C or 1065 | Form 1120-S + K-1s | Form 1120 |

Complexity | Low | Moderate | High |

One important note: electing S corp status does not change your LLC's legal structure. Your LLC stays an LLC at the state level. Only the federal tax treatment changes. This is a popular route for business owners who want the flexibility of an LLC and the tax efficiency of S corp treatment.

For a detailed look at how these structures compare for your specific situation, the C Corp vs. S Corp vs. LLC guide walks through the trade-offs in practical terms.

Who Should Elect S Corp Status in 2026?

S corp status is not a universal upgrade. It makes financial sense for some businesses and not others. The deciding factor is almost always income level. Here is the practical framework:

Strong case for S corp election:

- Net profit consistently above $75,000–$80,000 per year

- You work actively in the business (owner-employee)

- Your business is domestic, with U.S.-based ownership

- You plan to stay under 100 shareholders for the foreseeable future

Weaker case for S corp election:

- Net profit below $60,000 (ongoing costs may offset savings)

- Income is variable or seasonal — hard to set a reasonable salary

- You plan to bring in foreign investors or raise venture capital

- You want to avoid the complexity of running payroll

Specific Business Profiles

The freelance consultant making $100,000+:

With low overhead and high margins, a consultant netting six figures is often a strong candidate. Payroll tax savings on distributions above a reasonable salary can easily exceed the administrative costs of maintaining the structure.

The family-owned service business:

A home services company, accounting firm, or retail operation with consistent annual profits above $80,000 often benefits from S corp status. Multiple family members can be shareholders, and distributions flow through cleanly.

The real estate investor:

This one requires more nuance. Passive rental income is generally not subject to self-employment tax, regardless of entity structure, so the primary S corp benefit may not apply. Active real estate professionals like agents, developers, and property managers are different. A tax professional familiar with real estate taxation should weigh in before electing.

The early-stage startup:

Generally not the right time. If profits are inconsistent, the added costs and compliance requirements are hard to justify. Build the business first. Revisit the structure when profit stabilizes.

Not sure which path fits your business? Our S Corp vs. LLC comparison goes deeper into how each structure plays out across different business types.

What Happens If You Lose S Corp Status?

S corp status is not permanent by default. The IRS can terminate it, or you can inadvertently lose it if your business stops meeting eligibility requirements.

Common triggers for termination include:

- Exceeding 100 shareholders

- Bringing on a foreign (non-U.S. resident) shareholder

- Issuing a second class of stock

- Transferring shares to an ineligible entity, such as a C corp or partnership

- Failing to meet the domestic corporation requirement

What Happens After Termination

If S corp status is terminated involuntarily, the business reverts to C corp tax treatment starting the day the violation occurred. That can create a complicated tax situation; some income is taxed as pass-through, some as corporate income.

Voluntary termination requires a formal revocation filed with the IRS, signed by shareholders holding more than 50% of the stock. Once terminated, the IRS generally does not allow re-election of S corp status for five years.

The Takeaway: Set up eligibility controls early. If you plan to bring in investors, grow your shareholder base, or consider foreign ownership, understand those boundaries before crossing them.

The True Cost of Running an S Corp

Annual Operating Costs You Should Plan For

One of the most important questions to ask before electing S corp status: What will this actually cost me each year?

Here is a realistic breakdown:

Cost Item | Estimated Annual Range |

Payroll service (e.g., Gusto, ADP) | $400–$1,800 |

Form 1120-S tax preparation | $800–$2,000+ |

Bookkeeping (if outsourced) | $1,200–$3,600 |

State filing fees/franchise taxes | Varies by state |

Total estimated annual cost | $3,500–$6,000+ |

California adds a 1.5% franchise tax on S corp net income at the state level. New York has its own set of minimum taxes. Always research your specific state's rules before making the decision.

The Break-Even Calculation

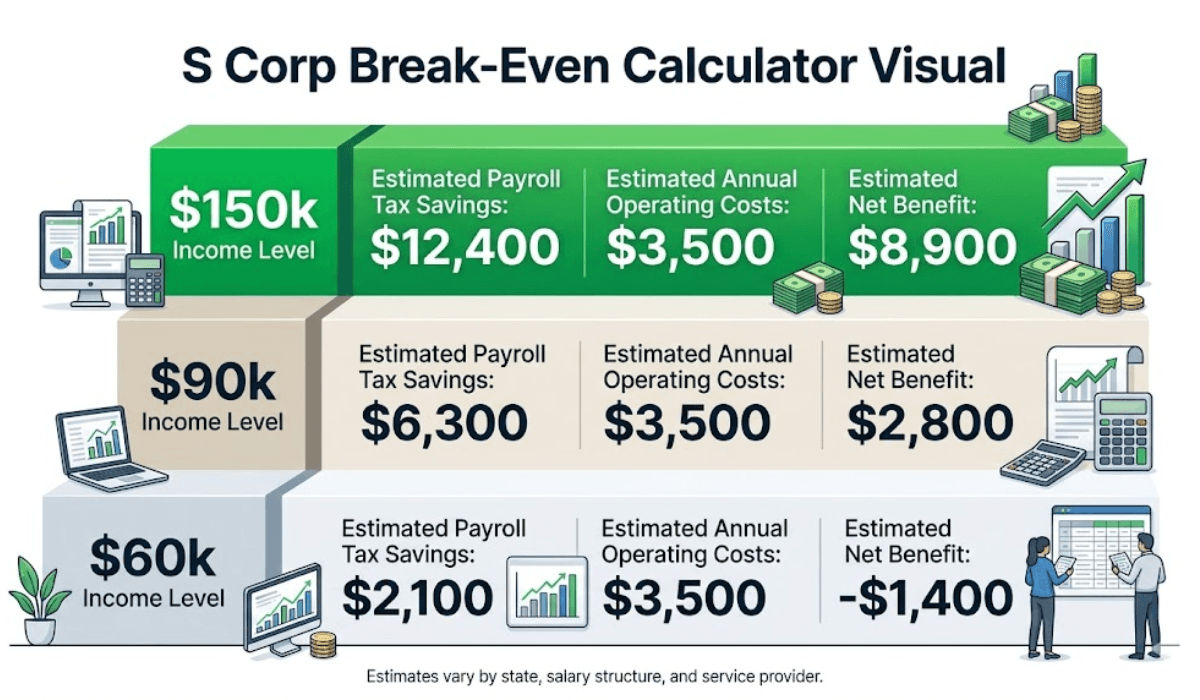

At $60,000 in net profit with a $40,000 salary, payroll tax savings are roughly $3,060. If annual costs come to $4,000, the math does not work yet.

At $90,000 in net profit with a $55,000 salary, savings are approximately $5,355. At that level, costs are covered, and there is a meaningful net benefit.

The break-even point for most businesses lands between $60,000 and $80,000 in annual net profit, depending on state, salary structure, and which services you use. Below that threshold, a default LLC is often the more cost-effective choice.

S Corp Benefits Beyond Tax Savings

Tax savings get most of the attention. But there are other meaningful advantages to S corp status worth knowing.

Limited Liability Protection

An S corp is a separate legal entity from its owners. That separation means your personal assets are generally protected from business debts and legal claims. This is the same protection an LLC provides, but it is worth restating for business owners currently operating as sole proprietors with no entity protection at all.

Business Credibility and Continuity

Operating as a corporation signals a level of commitment and permanence that sole proprietorships do not. Clients, vendors, lenders, and partners often view a registered corporation more favorably. Some contracts and lending programs are structured specifically for incorporated entities.

S Corps also have perpetual existence. If an owner dies or transfers shares, the business continues. That is not always the case with sole proprietorships or partnerships.

Easier Ownership Transfer

Transferring ownership interest in an S corp is generally cleaner than in a default LLC. Shares can be sold or gifted within the eligibility rules. There is no need to dissolve and reform the entity.

Health Insurance Deduction for Owner-Employees

S corp shareholders who own more than 2% of the stock are treated differently for health insurance than regular employees. The business can pay health insurance premiums for the owner, which are included in the owner's W-2 wages. The owner then deducts those premiums on their personal return as self-employed health insurance. [5]

This keeps the deduction — the net tax treatment is favorable — but the mechanics are different from what a non-owner employee experiences. If you currently pay your own premiums as a default LLC, this is worth reviewing with your tax professional.

Common Mistakes S Corp Owners Make With the IRS

Paying Yourself Too Little

This is the most common issue in S Corp returns. Some owners set salaries well below market rates to maximize distributions and minimize payroll taxes. The IRS watches for this specifically.

A salary of $30,000 on $300,000 in distributions will attract attention. Document your salary decision, benchmark it against industry data, and be prepared to defend it.

Missing Payroll Tax Deadlines

Once you run payroll, you have quarterly filing obligations. IRS Form 941 (Employer's Quarterly Federal Tax Return) is due four times per year. Form 940 (Employer's Annual Federal Unemployment Tax Return) is due annually. Missing these deadlines generates penalties. [6] [7]

A payroll service handles most of this automatically. It is one of the clearest cases where spending money on a service saves more in penalties and time.

Forgetting State-Level Compliance

S corp status is a federal tax election. Your state may have its own rules, fees, or taxes that apply. Some states do not recognize S corp status at all and tax the entity as a regular corporation. Others charge an additional franchise tax or minimum fee.

Review your state's specific requirements annually, especially if you operate across multiple states.

Not Keeping Corporate Records

S Corps, like all corporations, are expected to maintain records: meeting minutes, ownership records, and resolutions for major decisions. This is less intensive than it sounds, but neglecting it entirely weakens the legal separation between you and your business.

For more on what the S corp structure involves at a practical level, including the pros and cons of electing the Forming an S Corporation: Pros and Cons guide is a must-read.

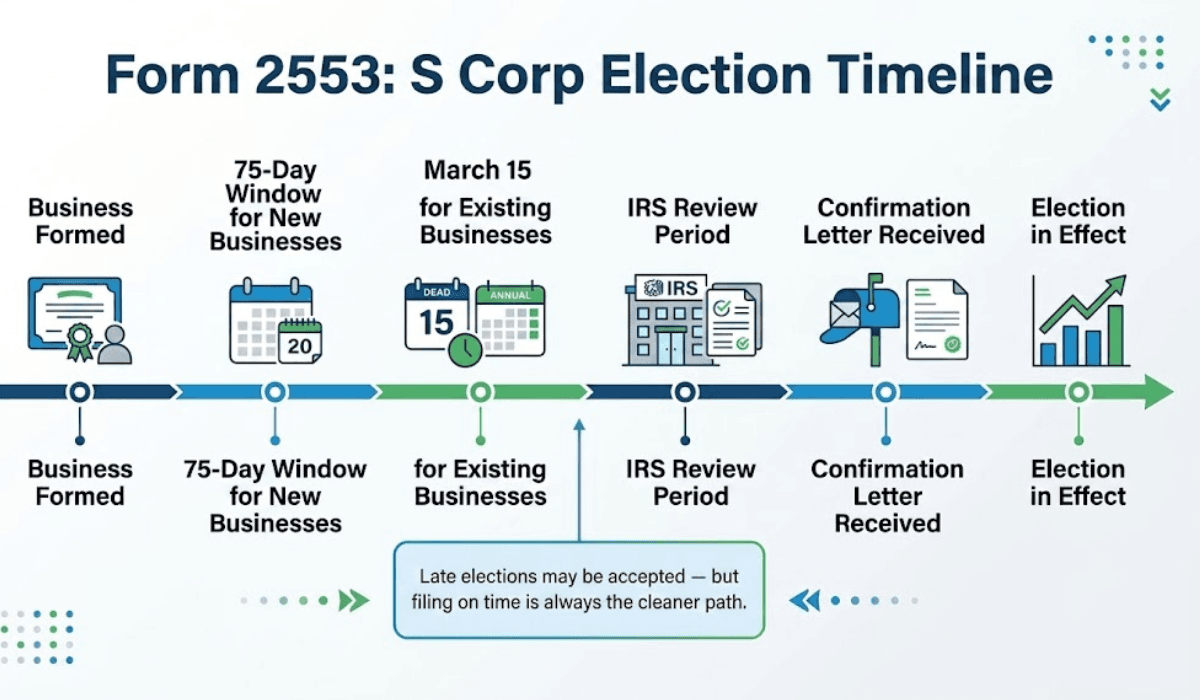

How to Elect S Corp Status: The Form 2553 Process

Electing S Corp status requires filing IRS Form 2553 (Election by a Small Business Corporation). [8] Here is how the process works:

Step 1: Confirm eligibility

Review the IRS requirements: domestic entity, 100 or fewer shareholders, one class of stock, U.S. citizens or resident shareholders only. Confirm your business meets all of them before filing.

Step 2: Get your EIN

You need an Employer Identification Number before filing. If you do not have one, apply through the IRS EIN application. [9]

Step 3: Complete Form 2553

The form requires: business name and address, EIN, tax year information, and the signatures of all shareholders consenting to the election.

Step 4: File on time

For an existing business, file by March 15 of the tax year you want the election to take effect. For a new business, file within 75 days of formation. Late elections can sometimes be accepted with reasonable cause, but filing on time removes the uncertainty.

Step 5: Receive IRS confirmation

The IRS will send a confirmation letter. If the IRS ever questions your status, that letter is your proof of election.

Step 6: Set up payroll

Once elected, you need to run payroll for yourself as an owner-employee. This means setting up a payroll system, withholding and remitting payroll taxes, and filing quarterly employment tax returns.

For a detailed walkthrough of each step, including LLC-specific considerations, the How to Start an S Corp Online guide walks through the full formation process.

Is an S Corp Right for You in 2026?

S corp status is a tax tool. Like any tool, it works well in the right conditions and adds unnecessary complexity in the wrong ones.

When you are ready to take the next step, Swyft Filings has helped 600,000+ businesses move forward with confidence. Our business formation specialists can walk you through the process, help you file an S Corp, and make sure your structure is set up right from the start.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Consult a licensed professional for guidance specific to your situation.

Bibliography

- Internal Revenue Service. S Corporations. Accessed May 15, 2026.

- Internal Revenue Service. About Form 1120‑S, U.S. Income Tax Return for an S Corporation. Accessed May 15, 2026.

- Internal Revenue Service. Qualified Business Income Deduction. Accessed May 15, 2026.

- U.S. Bureau Of Labor Statistics. Occupational Employment and Wage Statistics. Accessed May 15, 2026.

- Internal Revenue Service. Guide to business expense resources. Accessed May 15, 2026.

- Internal Revenue Service. About Form 941, Employer’s Quarterly Federal Tax Return. Accessed May 15, 2026

- Internal Revenue Service. About Form 940, Employer’s Annual Federal. Accessed May 15, 2026

- Internal Revenue Service. About Form 2553. Accessed May 15, 2026.

- Internal Revenue Service. Get an employer identification number. Accessed May 15, 2026.