Many LLCs in the United States generate little or no revenue in their first year, yet they may still have tax filing obligations. Wonder why? Let's find out.

A record-breaking 5.62 million business applications were lodged in the U.S. in 2025. So far in 2026, business applications are up 17.37% compared to the same period last year, with 2.02 million applications through the first four months of 2026 vs. 1.72 million in 2025 [1]

While many of these new LLCs spend their first year building a product or brand with zero revenue, the IRS still considers them "open for business." Even if your LLC made exactly $0 last year, you still have tax obligations. What you file and what you owe depend on how your LLC is taxed and which state it is registered in.

Missing these zero-income filings can result in penalties ranging from several dollars a month to the automatic dissolution of your company by the state. This guide breaks down exactly which forms to file for 2026 and how to protect your liability.

Key Takeaways

Your LLC's tax filing obligation is based on its IRS classification, not whether it made money.

Multi-member LLCs must file Form 1065 annually; failing to file it triggers a $ 255-per-partner-per-month penalty.

Single-member LLCs with no income and no expenses have no separate filing requirement.

California's $800 franchise tax and other state fees are owed regardless of revenue.

Startup costs up to $5k can be deducted under IRC Section 195, even in a zero-income year.

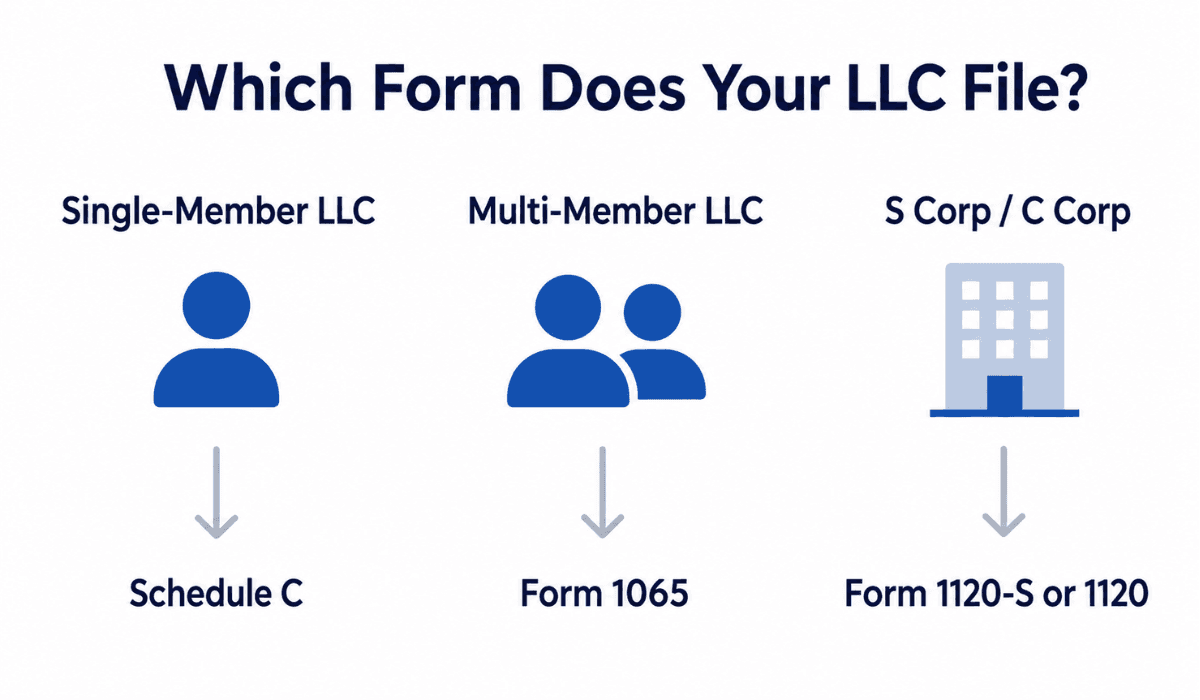

Step 1: Know Your LLC's Tax Classification

Before you can file anything, you need to know how the IRS classifies your LLC. This determines which forms you file.

LLC Type | Default IRS Classification | Primary Federal Form |

Single-member LLC | Disregarded entity (sole proprietor) | Schedule C (with Form 1040) [2] |

Multi-member LLC | Partnership | Form 1065 [3] |

LLC taxed as an S corporation | S corporation | Form 1120-S [4] |

LLC taxed as a C corporation | C corporation | Form 1120 [5] |

If you filed IRS Form 8832 to be classified as a corporation (C corp), you file as a C corporation. If you filed Form 2553 to elect S corporation status, you file as an S corporation. If you filed neither, your LLC follows its default classification. [6] [7]

Not sure which applies to you?

Check your IRS confirmation letters from when you applied for your EIN, or ask your business formation specialist, if you have one.

Step 2: File the Correct Federal Forms

Single-Member LLC (Disregarded Entity)

A single-member LLC that made no income still reports on the owner's personal tax return.

- File Form 1040 with Schedule C attached

- Report zero income on Schedule C

- You may still deduct legitimate business expenses incurred during the year, even with no revenue

- Due date: April 15, 2026 (for the 2025 tax year)

If you need more time, file Form 4868 for an automatic 6 month extension to October 15, 2026. This extension gives you more time to file, not more time to pay any tax owed. If you owe the state any money from your personal income, interest on any unpaid balance begins accruing regardless of the extension. [8]

Multi-Member LLC (Partnership)

Every multi-member LLC taxed as a partnership must file Form 1065, even with zero income.

- File Form 1065 (U.S. Return of Partnership Income)

- Provide Schedule K-1 to each member and attach to Form 1065 [9]

- Report zero income and any deductible expenses

- Due date: March 17, 2026 (for the 2025 tax year, since March 15 falls on a Sunday)

For the 2026 tax season covering the 2025 tax year, the IRS late filing penalty for Form 1065 is $255 per partner per month the return is late. A two-member LLC filing three months late owes $1,530 in penalties on a return with zero income.

File Form 7004 by March 17 to get an automatic 6 month extension to September 15, 2026. [10]

LLC Taxed as an S Corporation

- File Form 1120-S (U.S. Income Tax Return for an S Corporation)

- Provide Schedule K-1 to each member and attach to Form 1065

- Report zero income and track any shareholder distributions or losses

- Due date: March 16, 2026 (for the 2025 tax year, since March 15 falls on a Sunday)

For 2026, the late filing penalty is $235 per shareholder per month. A two-owner S Corp filing three months late could incur $1,410 in penalties ($235 × 2 shareholders × 3 months.

File Form 7004 by March 16 to get an automatic 6 month extension to September 15, 2026.

LLC Taxed as a C Corporation

- File Form 1120 (U.S. Corporation Income Tax Return)

- Report zero income and document startup expenses as Net Operating Losses (NOLs)

- Carry Forward Losses: Filing allows you to "lock in" these expenses to offset your future profits when the business grows.

- Due date: April 15, 2026 (for the 2025 tax year)

File Form 7004 by April 15 to get an automatic 6 month extension to October 15, 2026.

Step 3: Check Your State Requirements

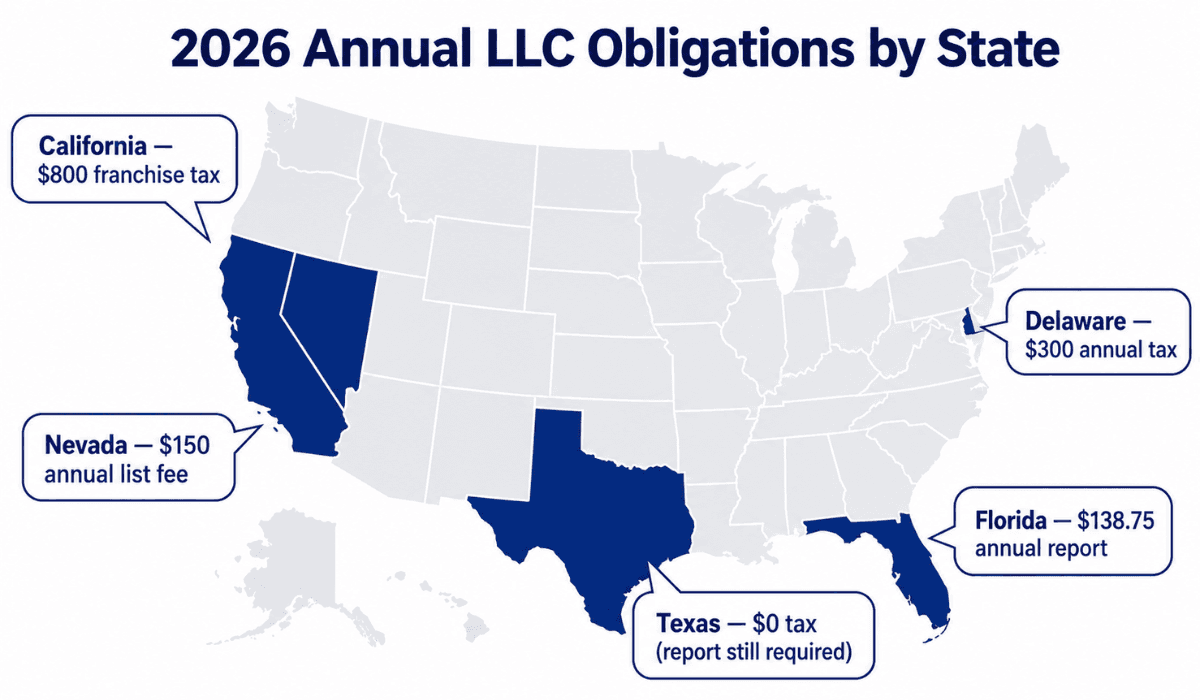

Federal filing is only part of the picture. Every state has its own rules for LLCs, and most charge fees regardless of income. Here are the states that carry the heaviest obligations for zero-income LLCs.

High-obligation states to know:

State | Key Obligation | Amount |

California | Annual franchise tax | $800 minimum, due every year until the LLC is formally canceled [11] |

Delaware | Annual franchise tax | $300, due June 1 each year [12] |

Massachusetts | Annual report + excise tax | $500 filing fee + $456 minimum excise [13] |

Tennessee | Franchise tax | $300 minimum [14] |

Maryland | Personal property return | $300 flat minimum [15] |

Texas | Franchise tax report | $0 owed if under $2.47M in revenue, but the report must still be filed [16] |

States like Wyoming ($60/year), South Dakota ($50/year), and Colorado ($10/year) are the most favorable for dormant LLCs. [17] [18] [19]

Most states fall somewhere in between, with annual or biennial report fees ranging from $15 to $150. Check with your state's Secretary of State or Department of Revenue for the current requirements.

Step 4: Deduct Your Business Expenses

Zero income does not mean zero deductions. If your LLC spent money during the year on legitimate business costs, those expenses are deductible even with no revenue.

Common deductible expenses for no-income LLCs include:

- LLC formation fees and state filing costs

- Business software subscriptions

- Website hosting and domain registration

- Legal and accounting fees

- Home office expenses

- Business mileage at the 2026 IRS standard rate of 70 cents per mile

Under IRC Section 195, you can deduct up to $5,000 in startup costs in the year you begin business. Any remaining startup costs above the deductible threshold are generally amortized over 180 months. [20]

A net loss from these expenses carries forward and offsets future income once your LLC becomes profitable. Keep records for everything, even in a zero-revenue year.

Step 5: Decide Whether to Keep the LLC or Dissolve It

If your LLC has been inactive and you have no plans to use it, you have two options. File the required returns each year to keep it alive, or dissolve it and stop the obligations entirely.

Keeping a dormant LLC alive makes sense if you plan to use the entity in the future, want to protect the business name, or have contracts or intellectual property tied to the LLC.

Dissolving makes sense if you are certain you will not use the entity again, if the annual costs outweigh the benefit, or if you want to stop the state and federal filing clock permanently.

Dissolving an LLC is not simply stopping to pay fees. You must file formal articles of dissolution with your state's Secretary of State office and settle any outstanding taxes. Some states also require a final tax return to close the LLC's account with the state revenue department.

If you are on the fence, consider keeping the LLC alive for one more year while you decide. The cost of dissolving and then re-forming a new LLC later can exceed a few years of annual fees.

Next step: If you are leaning toward dissolution, read our guide on Why You Should Dissolve an Unused Business Before Year’s End to understand the exact steps before you decide.

What Happens If You Don't File?

Missing a filing when your LLC has no income does not mean you get a pass. The consequences stack up in three ways.

IRS Penalties

For a multi-member LLC, the IRS assesses a penalty under IRC § 6698 of $255 per partner per month for returns due after December 31, 2024, for up to 12 months. This penalty applies even if the partnership had no income, no expenses, or no tax due for the year.

For a single-member LLC filing as a disregarded entity, the penalty for failing to file Schedule C is tied to the underlying Form 1040 late filing penalty, typically 5% of any tax owed per month, up to 25%.

State Penalties and Dissolution

Most states impose late fees on annual reports and returns. More seriously, many states will administratively dissolve your LLC if you miss filings for one to three consecutive years. Dissolution means:

- You lose your liability protection immediately

- You may lose the right to use your LLC name

- You may face personal liability for business debts incurred after dissolution

- Reinstating a dissolved LLC requires back fees, penalties, and paperwork

Loss of Good Standing

Even before dissolution, missing filings put your LLC "not in good standing." That status can block you from opening business bank accounts, winning contracts, getting financing, or registering in other states.

Takeaway:

Staying compliant is essential, even when your LLC has no income. If managing tax filings and annual reports feels overwhelming, professional compliance support can help reduce the risk of costly penalties. Let the business formation experts at Swyft Filings handle your formation, annual reporting, and compliance management so you can focus on growth.

Note: All due dates, penalty rates, and fee amounts in this guide apply to U.S.-registered LLCs filing returns for tax year 2025 in 2026, unless otherwise noted.