Swyft's Resource Center

Browse Blogs by Category

C Corporation

Read up-to-date articles on C-Corp incorporation, bylaws, shares, and ongoing requirements.

View Detail

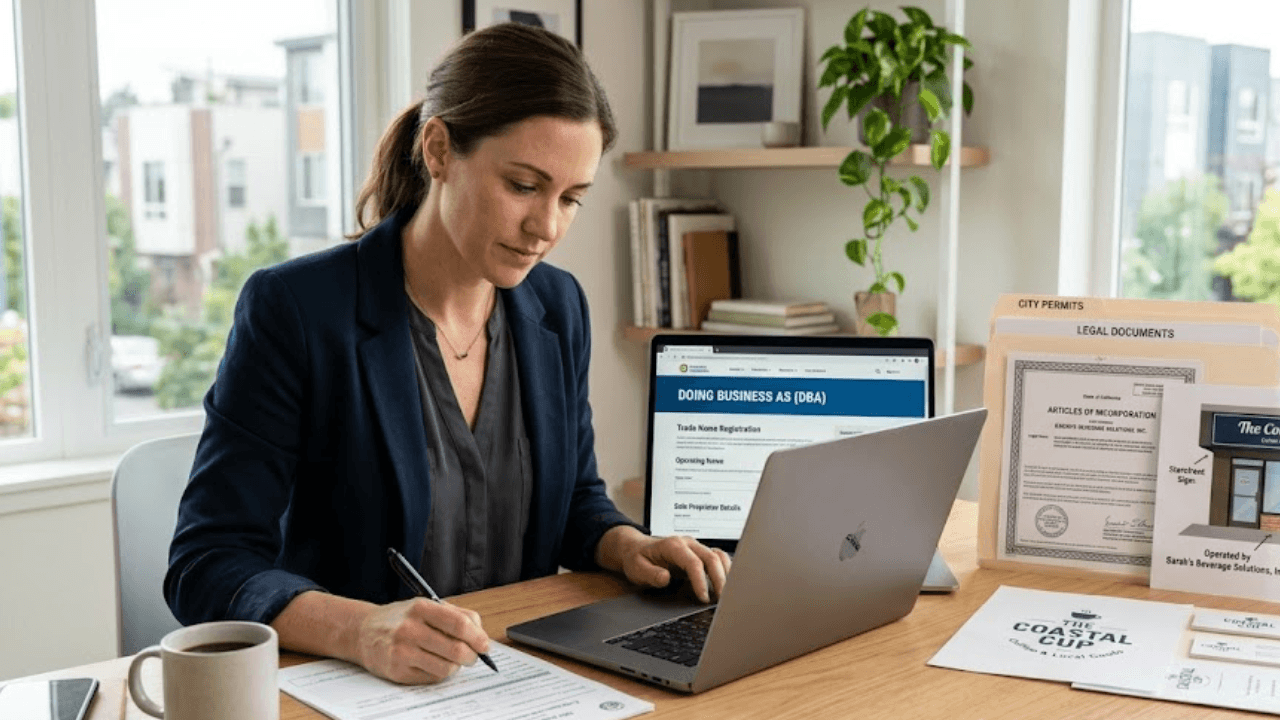

DBA

Know how to file a new business name for your existing business and how it works for an LLC or corporation.

View Detail

LLC

Start smart with LLC guides that explain setup, costs, and state rules in easy words.

View Detail

Non Profit

Learn all about paperwork, timelines, and common mistakes to avoid while forming a Non-Profit.

View Detail

S Corporation

Follow our practical guides on S-Corp formation eligibility, Form 2553, and tax basics.

View Detail

Most Trending Blogs

What is a Sole Proprietorship?

A sole proprietorship is a one-person business with no legal separation between the owner and the entity, offering total control but 100% personal liability risk. Keep reading for more!

Read more

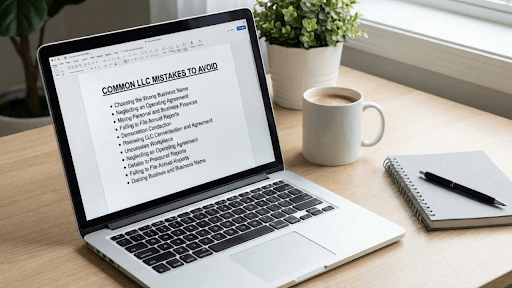

15 Common LLC Mistakes to Avoid in 2026 (And How to Avoid Them)

Avoid costly mistakes when starting or managing an LLC in 2026. This guide covers 15 common LLC errors and practical ways to stay compliant, protected, and on track.

Read more

State-Specific LLC Filing Requirements (2026 Guide)

Form your LLC hassle-free with state-specific filing requirements! Get help with formation, EIN, operating agreements, and ongoing compliance. Start now!

Read more

Latest Blog Posts

10 Marketing Tips Every New Business Owner Should Do First

You just formed your business. Now what? These 10 beginner-friendly marketing tips will help new business owners attract their first customers, build their brand, and grow with confidence.

Read more

Is It Worth Using an LLC Filing Service in 2026?

An LLC filing service saves time and helps avoid paperwork mistakes, but whether you need one depends on your budget and compliance needs.

Read more

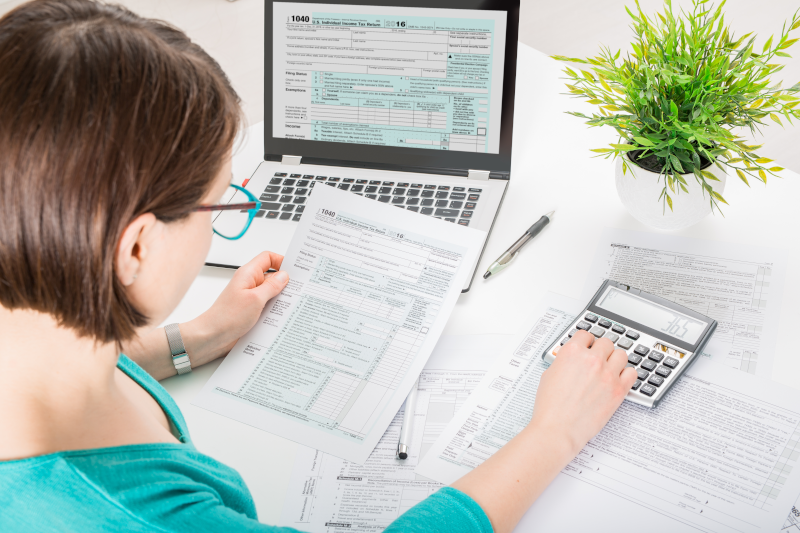

How To File Taxes for an LLC With Zero Income (2026 Guide)

Many LLCs in the United States generate little or no revenue in their first year, yet they may still have tax filing obligations. Wonder why? Let's find out.

Read more

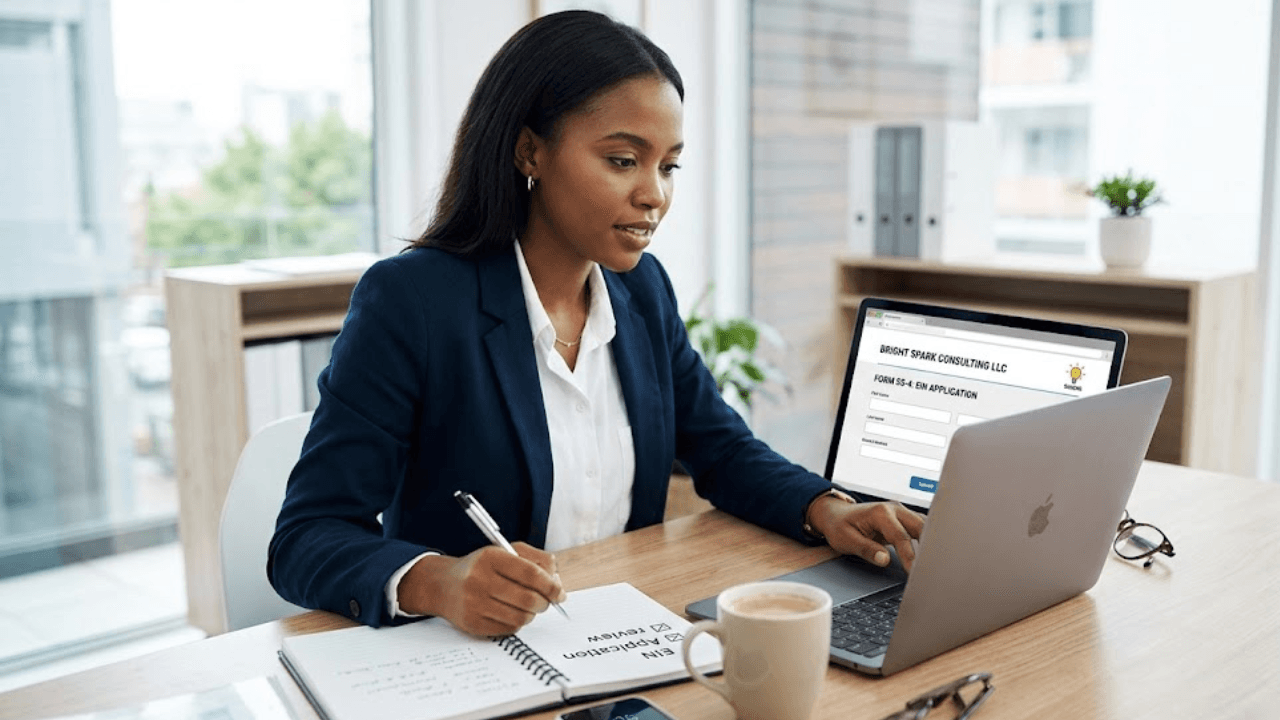

What Is an EIN? The Complete Guide for Small Business Owners (2026)

An Employer Identification Number (EIN) is a unique nine-digit number the Internal Revenue Service (IRS) assigns to businesses in the United States.

Read more

What Is a Registered Agent? Everything You Need to Know

A registered agent is an individual or entity officially appointed in your state of formation to receive legal notices, lawsuits, and government correspondence on behalf of your business.

Read more

What Is a Nonprofit Organization? A Complete Guide (2026)

A nonprofit organization (NPO) is a legal entity formed to advance a mission, social, educational, charitable, religious, or public, rather than to generate profits for owners or shareholders.

Read more

A Complete S Corp Tax Guide: How to Save More in 2026

You have built a business that is actually making money. Now every dollar of profit gets hit with a 15.3% self-employment tax before you see a cent of it. But there is a way to change that.

Read more

What Are the Different Types of LLCs?

There are 9 types of LLCs. Each one serves a different business need. Most small business owners will choose between a single-member or multi-member LLC, and everything else is specialized from there.

Read more

What is a Sole Proprietorship?

A sole proprietorship is a one-person business with no legal separation between the owner and the entity, offering total control but 100% personal liability risk. Keep reading for more!

Read more

What Is an EIN Filing Service?

An EIN is your business's tax ID number issued by the IRS. An EIN filing service handles the application process for you, accurately and quickly.

Read more

Swyft Filings Business Resources Made Simple

Helpful articles and trusted guidance to help you form your business, stay compliant, and keep growing with confidence

Top 10 Ways to Choose the Right Registered Agent Service

Jeff Mosler

Jun 25, 2026

Choosing the right agent registered to represent your business is one of the most impactful decisions you will make as an entrepreneur. A reliable registered agent is not just a compliance requirement—this partner ensures your company’s legal standing, privacy, and delivers business compliance services that are critical to your ongoing success. Whether you’re looking for an LLC registered agent, searching for registered agent service for LLC, considering statutory agent services, or comparing providers like Swyft Filings and other registered agents Inc, your choice will affect your peace of mind and business operations.

![Small Business Grants for Women-Owned Businesses [2026 Guide]](https://cms.360legal.com/assets/Small_Business_Grants_for_Women_Owned_Businesses_cef399a026.png)

![15 Common Business Models for First-Time Entrepreneurs [2026 Guide]](https://cms.360legal.com/assets/Common_Common_Business_Models_for_First_Time_Entrepreneurs_Business_Models_for_First_Time_Entrepreneurs_ee09bf0058.png)

Go-to stories from our writers

Learn from the team that's helped 600,000+ businesses get it right from day one. Read the insights you need to form your business with confidence—straight from our team.

How to Get a Registered Agent in South Carolina

How to Get a Registered Agent in Alabama

How to Get a Registered Agent in Vermont

2019 Swyft Filings State of the Industry Report

The Swyft Filings State of the Industry Report provides an examination of business formation trends by looking at the number of newly-created businesses by industry type between 2018 and 2019.

LLC vs INC: The Great Business Structure Debate

Requirements All Amazon Sellers Should Know About

How to Get a Registered Agent in North Carolina

How to Get a Registered Agent in Oregon

How to Convert a DBA to an LLC

You cannot technically "convert" a DBA into an LLC. Because a DBA is simply a registered pseudonym or "fictitious name" for an existing business or individual.

Can An LLC Be A Nonprofit? How To Convert To A 501(c)(3)

Shifting from a profit-driven LLC to a purpose-led 501(c)(3) requires a strategic legal pivot. Learn how to reconstruct your entity and secure tax-exempt status.

Starting a Business in South Carolina: 8 Essential Steps

How to Apply for an EIN (Employer Identification Number)

An EIN is a nine-digit federal tax ID that every registered business needs to operate, bank, and hire legally. Applying is free and takes just minutes online.

How to Switch From Sole Proprietor to LLC (What Nobody Tells You)

Switching from a sole proprietorship to an LLC affects more than your business name. It may require a new EIN and impact your bank account and contracts.

ZenBusiness vs. LegalZoom: Comparing LLC Formation Services (2026 Update)

In 2026, the comparison between ZenBusiness and LegalZoom is not just about filing an LLC, but also about cost, speed, compliance services, add-ons, etc.

Incfile vs. LegalZoom: Comparing LLC Formation Services

We've compared Incfile vs. LegalZoom across every point that matters to a first-time founder, like pricing, filing speed, compliance tools, and more. Keep reading!

Verify Your Business Name With an Illinois Business Name Search

Prepare to incorporate your Illinois business by running a business entity search. This free search will help you choose an available name.

Verify Your Business Name With a Connecticut Business Name Search

Narrow down your options for a unique, compliant Connecticut business name with a free entity search. Perform this necessary search before incorporating.

Verify Your Business Name With a Missouri Business Name Search

A free, online Missouri business entity search will check the availability of potential business names. Confirming your name will save you money and time in the incorporation process.

10 Marketing Tips Every New Business Owner Should Do First

You just formed your business. Now what? These 10 beginner-friendly marketing tips will help new business owners attract their first customers, build their brand, and grow with confidence.

Nonprofit Formation Checklist: Steps to Take After Starting a Nonprofit

Forming your nonprofit is an important milestone. This checklist helps you stay organized, meet requirements, and prepare for long-term impact.

What Is a DBA? A Complete Guide to Doing Business As

You want your business to have a real name. A name people can find, trust, and pay. But the paperwork seems confusing. That is where a DBA comes in.

Swyft Filings Vs. LegalZoom: Which LLC Formation Service Is Right For You?

Swyft Filings and LegalZoom are both business formation services, but they're built for very different buyers. Our review compares their LLC services in detail!

Tailor Brands Vs. LegalZoom For LLC Formation In 2026

We compared Tailor Brands vs LegalZoom based on pricing, filing speed, customer support, and other features so you can make an informed choice.

What is a Sole Proprietorship?

A sole proprietorship is a one-person business with no legal separation between the owner and the entity, offering total control but 100% personal liability risk. Keep reading for more!

How Much do the "Twelve Days of Christmas" Cost in Your State?

To estimate the cost of all gifts listed in the "Twelve days of Christmas" by state, Swyft Filings referred to the most recent data from small businesses, the Bureau of Economic Analysis, and the Bureau of Labor Statistics.

The Best City in Each State to Start a Business

Based on the most recent data, these are the best cities in each state to start a new business.

Entrepreneurship Hotspots of the United States: The Top Cities Encouraging New Business Growth (2023)

The appeal of starting a business is substantial anywhere, but its location can often play a pivotal role in its survival and success.

How to Get a Registered Agent in Pennsylvania

It’s essential to fulfill your Pennsylvania registered agent requirements and stay compliant with the Secretary of State.

Should Artists Start an LLC?

An artist should consider forming an LLC once their creative work moves beyond casual sales and involves real business risk. But how do you know when you've reached that tipping point?

9 Green Small Business Ideas You Can Start Today

LLC Operating Agreement: What It Is and How to Create One

An LLC operating agreement sets rules for ownership, management, and profits, protecting personal assets and preventing disputes.

Starting a Business in Florida: 8 Essential Steps

Do Single Member LLCs Need Operating Agreements?

How To Change A Registered Agent For An LLC Or Corporation

If your current registered agent setup feels messy, unreliable, or too exposed, changing it is one of the simplest ways to regain control.

On the Rise: These Cities Have the Highest Potential for New Business Growth

With just the right combination of factors, these are the cities where future business ventures are expected to thrive.

States With the Most Jobs Created by New Businesses

Vital to the growth and revitalization of their industries and communities, new businesses have created the most jobs in these ten states.

Top 10 Ways to Start Your Business and Form an LLC

Ready to start your business by forming an LLC or corporation? Starting an LLC online is simpler than ever, whether it's for a fresh idea or to grow what you have. Folks forming an LLC today seek business protection, management flexibility, and trust. Let’s explore the top 10 ways to start and LLC, create an LLC online, and navigate every step from LLC application through LLC registration. This actionable guide will help your company stand out with leading LLC formation and incorporation services.

Top 10 Ways to Choose the Right Registered Agent Service

Choosing the right agent registered to represent your business is one of the most impactful decisions you will make as an entrepreneur. A reliable registered agent is not just a compliance requirement—this partner ensures your company’s legal standing, privacy, and delivers business compliance services that are critical to your ongoing success. Whether you’re looking for an LLC registered agent, searching for registered agent service for LLC, considering statutory agent services, or comparing providers like Swyft Filings and other registered agents Inc, your choice will affect your peace of mind and business operations.

States with the Largest Job Increases Over the Last 20 Years

How many jobs has your state's economy added in the last two decades? Relying on the most recent federal data, Swyft Filings ranked all 50 states and Washington D.C.

Cities with the Most Competitive Office Lease Markets

Despite higher interest rates, a slowing economy, and shifting work habits, the office lease market in these 35 cities remains strong.

Best States to Start a Nonprofit

How to Apply for a Second Round PPP Small Business Loan

Book Your Free Consultation Or Call Today!

Don’t waste time with anyone else. Call us first, and we will help you seek fair and just compensation.