Your business structure affects your taxes, ownership, liability protection, and many other important parts of your business. That’s why choosing the right structure can feel confusing and often take

Key Takeaways

he most common business structures in the United States are sole proprietorships, partnerships, limited liability companies (LLCs), corporations, and nonprofits.

Each structure has different rules for taxes, liability protection, ownership, and management.

For many small business owners, an LLC offers a balance of personal asset protection and flexibility. However, the right choice depends on your goals, industry, ownership structure, and future plans.

The most common business structures people choose in the U.S. are sole proprietorships, partnerships, LLCs, S corporations, C corporations, and nonprofits, all of which work differently. Each one has its own benefits, limits, and use cases.

The good news is that choosing a structure becomes easier when you understand what each option is designed to do. That's what we will be discussing in this blog.

Keep reading for more.

Business Structure Comparison At a Glance

Business Structure | Liability Protection | Tax Treatment | Number of Owners | Complexity | Best For |

Sole Proprietorship | No separate liability protection | Reported on the owner’s personal tax return | 1 | Low | Freelancers, side hustlers, and solo owners testing an idea |

Partnership | Depends on partnership type | Pass-through taxation | 2 or more | Low to moderate | Businesses with multiple owners |

Yes, when properly maintained | Flexible tax options | 1 or more | Moderate | Small businesses, consultants, e-commerce sellers, agencies | |

Yes, when properly maintained | Pass-through taxation | Up to 100 shareholders | Moderate | Growing businesses that meet S Corp rules | |

Yes, when properly maintained | Corporate taxation | Unlimited shareholders | Higher | Startups seeking investors or issuing stock | |

Generally yes | May qualify for tax-exempt status | Board governed | Moderate to higher | Charitable, educational, or mission-driven organizations |

How to Choose the Right Business Structure

A structure that works well for a freelance graphic designer may not be the right choice for a technology startup seeking investors. Likewise, a local retail shop may have different needs than a nonprofit organization or an online business.

The SBA recommends choosing a structure that gives you the right balance of legal protections and benefits. It also notes that business structure can affect taxes, paperwork, money raising, and personal liability. [1]

As you compare your options, focus on five key factors.

1. Personal Liability Protection

Liability protection determines whether your personal assets remain separate from your business obligations.

With a sole proprietorship, there is generally no legal separation between you and your business. With structures such as LLCs and corporations, the business is treated as a separate legal entity, which can help create an additional layer of protection when operated properly.

For many entrepreneurs, liability protection is one of the main reasons they move beyond a sole proprietorship.

2. Tax Treatment

Different business structures are taxed differently.

Some structures use pass-through taxation, where profits and losses flow directly to the owners' personal tax returns. Others are taxed at the business level.

Certain structures may also offer additional flexibility through tax elections.

Understanding how taxes work can help you evaluate both short-term and long-term implications for your business.

3. Ownership Structure

Ask yourself:

- Will you be the only owner?

- Will you have business partners?

- Do you plan to bring on investors?

Some structures have few ownership restrictions, while others have specific rules regarding shareholders and ownership interests.

4. Administrative Requirements

Every business structure comes with responsibilities.

Some require very little ongoing administration. Others involve annual filings, recordkeeping obligations, shareholder meetings, or additional reporting requirements.

The right choice often balances protection and flexibility with the amount of administration you're comfortable managing.

5. Future Growth Plans

Think about where your business could be in three to five years.

If you expect to remain a solo business owner, your needs may differ from those of someone planning to hire employees, expand nationally, or seek outside investment.

Choosing a structure that supports your future goals can help reduce friction as your business grows.

What Are The Different Types of Business Structures

There are 6 main types of business structures. Each serves a different purpose. Below is an overview of the most common options.

Sole Proprietorship

A sole proprietorship is the simplest business structure.

When one person starts a business and does not form a separate legal entity, the business is usually treated as a sole proprietorship by default.

A sole proprietorship can be easy to begin because it usually requires less paperwork than forming an LLC or corporation. The owner has full control over business decisions and typically reports business income on their personal tax return.

However, a sole proprietorship does not create a legal separation between the owner and the business. That means the owner and the business are treated as closely connected.

This structure may work well for someone testing a new idea or earning income on the side. As the business grows, some owners decide to explore an LLC for added structure, flexibility, and liability protection.

A sole proprietorship may be a fit for:

- Freelancers

- Independent contractors

- Side hustle owners

- Solo service providers

- New business owners testing an idea

Next step: Compare sole proprietorships and LLCs to see when forming an LLC may make sense. For a deeper comparison, read Sole Proprietorship vs LLC.

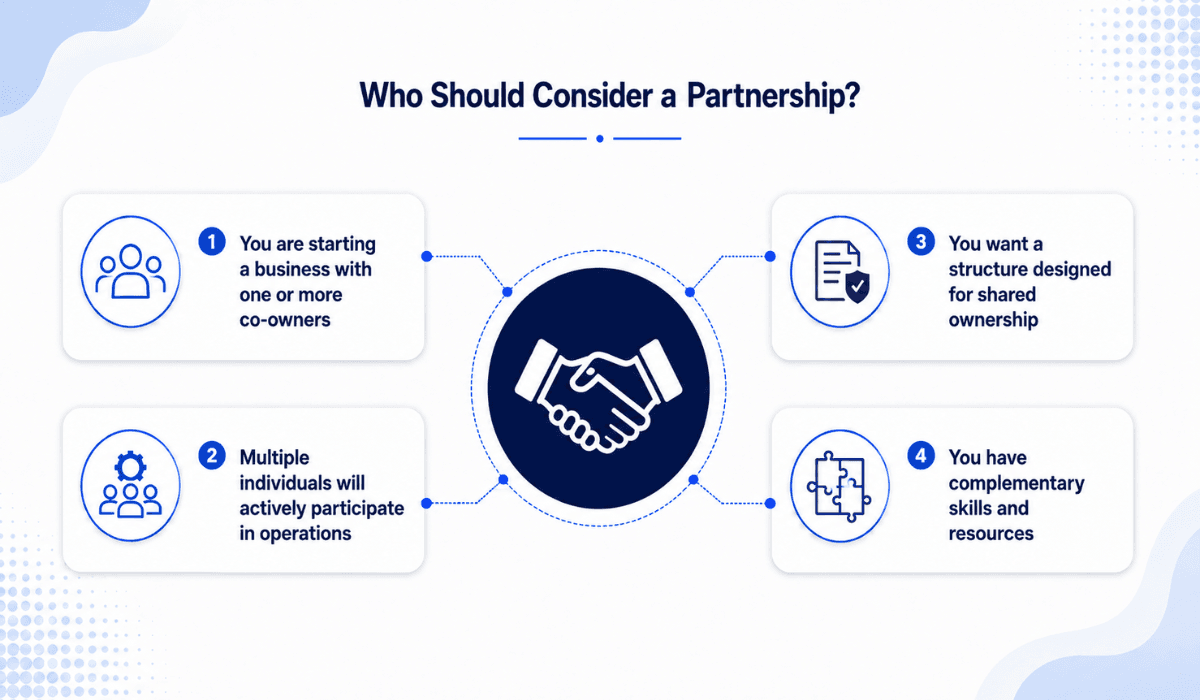

Partnership

A partnership is a business owned by two or more people.

Partnerships are often used when multiple owners want to share responsibilities, resources, skills, and profits. There are different types of partnerships.

- A general partnership is usually the simplest. In a general partnership, partners typically share business responsibilities and obligations.

- A limited partnership may include general partners who manage the business and limited partners who contribute capital but have a more limited role.

- Some professional businesses may consider a limited liability partnership, depending on state rules.

Partnerships can be helpful when owners bring different strengths to the business. For example, one partner may manage operations while another handles sales or finance.

The main challenge is that shared ownership requires clear communication. Partners should understand how profits, duties, decisions, and ownership changes will be handled.

A partnership tends to work well for:

- Family businesses

- Professional service firms

- Businesses with two or more active owners

- Owners combining capital, skills, or resources

Many business owners with partners also compare partnerships with LLCs because LLCs can support multiple owners while offering more structure and liability protection.

What helps most

If you choose a partnership, it is smart to create a written partnership agreement. This can explain ownership, profit sharing, roles, decision-making, and what happens if one partner leaves.

Limited Liability Company (LLC)

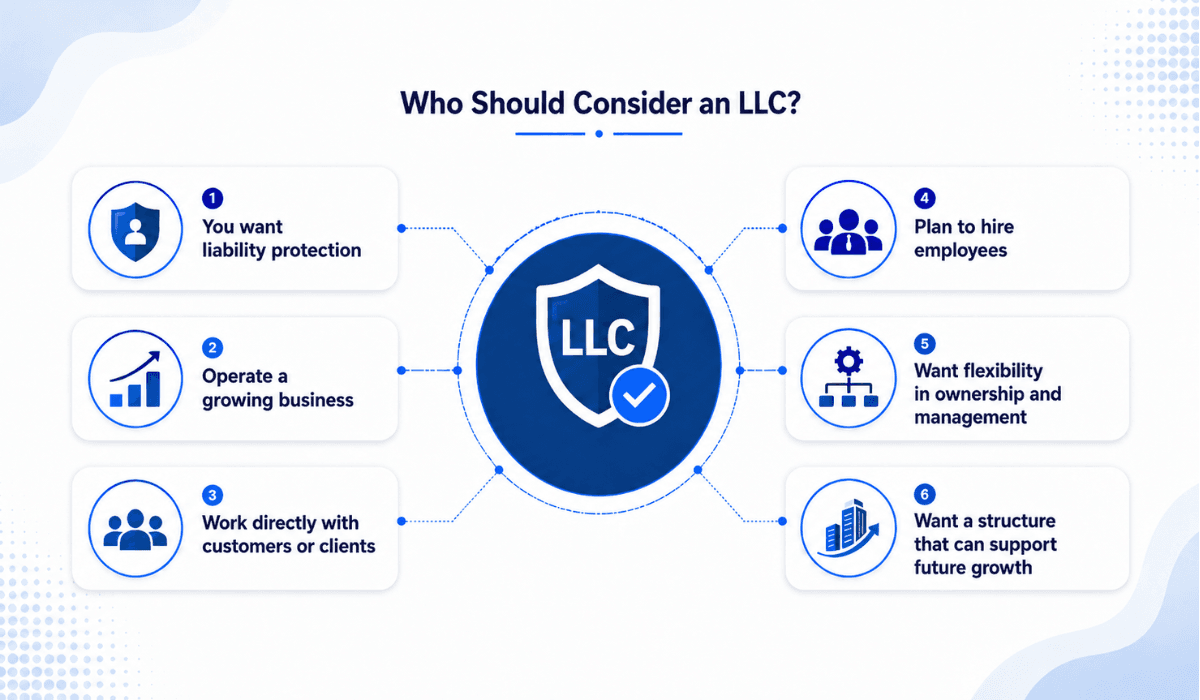

A Limited Liability Company, or LLC, is one of the most common business structures for small business owners.

An LLC is formed under state law and is generally treated as a separate legal entity from its owners. LLC owners are called members.

Many entrepreneurs choose an LLC because it offers a balance of liability protection, management flexibility, and tax flexibility.

An LLC can have one owner or multiple owners. A single-owner LLC is called a single-member LLC. An LLC with two or more owners is called a multi-member LLC. [2]

One reason LLCs are popular is that they can work for many types of businesses. Consultants, e-commerce sellers, agencies, contractors, local shops, and online business owners often consider forming an LLC as their businesses become more established.

An LLC may help business owners:

- Create a formal business structure

- Separate personal and business activities

- Add structure as the business grows

- Support flexible ownership

- Choose from different tax treatment options, depending on eligibility

Sole Proprietorship vs LLC: Quick Comparison

Factor | Sole Proprietorship | LLC |

Formation Process | Simple | Requires state filing |

Personal Liability Protection | Generally No | Yes |

Ownership | One owner | One or more owners |

Tax Flexibility | Limited | Flexible |

Administrative Requirements | Low | Moderate |

Growth Potential | Moderate | High |

For many small business owners, the decision often comes down to balancing simplicity with long-term business goals.

A sole proprietorship can be a practical way to start. An LLC can offer additional flexibility as a business grows.

Good next step

If you are leaning toward an LLC, compare your state’s filing fee, annual report rules, registered agent rules, and business license needs before you file.

For more details, read Swyft’s guides on State-Specific LLC Filing Requirements | LLC Tax Benefits | How To Start An LLC Online

S Corporation

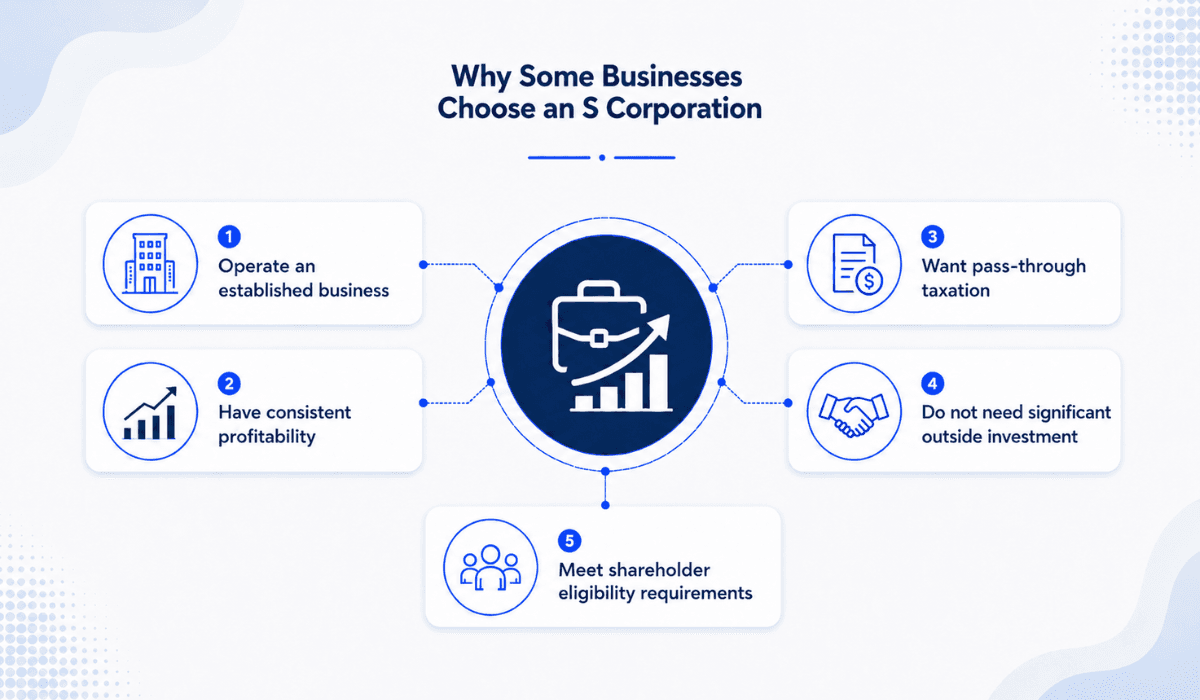

An S corporation is not a separate business entity formed at the state level. It is a federal tax election available to certain eligible businesses. An LLC or corporation may elect S Corp tax treatment if it meets the requirements.

S Corps are often chosen by more established businesses with steady revenue. This tax treatment may support certain planning goals, but it also comes with specific rules.

S Corps have ownership limits and may require more administrative work than a basic LLC. For example, owner-employees may need to be paid through payroll, and the business must follow S Corp eligibility rules.

S Corp election often makes sense for:

- Growing small businesses

- Businesses with steady profits

- Owners evaluating tax planning options

- Businesses that meet S Corp eligibility requirements [3]

Things to consider

S corporation rules are more limited than LLC rules. Ownership restrictions apply. Payroll, salary, and tax filing needs can also become more complex. Read our guides on What Is an S Corp and How To Start an S Corp Online for a deeper understanding.

C Corporation

A C Corporation, or C Corp, is a separate legal entity owned by shareholders.

This structure is often used by companies that plan to raise outside investment, issue stock, or grow into a larger organization.

C Corps can support unlimited shareholders and multiple classes of stock. This makes them attractive for startups seeking venture capital or businesses with more complex ownership goals.

A C Corp may also involve more formal requirements than an LLC or sole proprietorship. These may include corporate records, shareholder meetings, bylaws, and board governance.

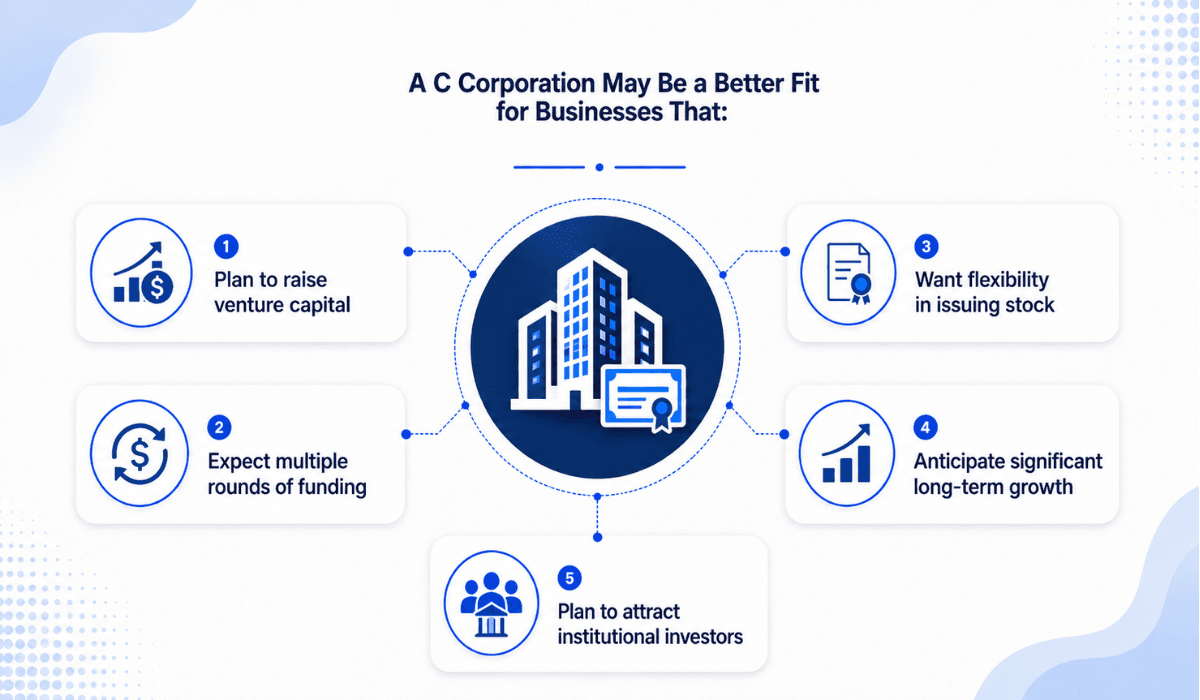

A C Corp is often the better fit for:

- Startups seeking investors

- Companies planning to issue stock

- Businesses with high-growth goals

- Companies preparing for multiple funding rounds

For many traditional small businesses, a C Corp may be more structured than they need at the beginning. For investor-backed companies, it may be the preferred path. [4]

Things to consider

C corporations usually require more paperwork, more formal records, and more structured governance than LLCs or sole proprietorships. To know more, read What is a C Corporation | C Corp Pros and Cons | LLC vs. Corporation and How to Start a C Corporation Online

Nonprofit Corporation

A nonprofit corporation is formed to serve a charitable, educational, religious, scientific, or community-focused purpose.

Unlike a for-profit business, a nonprofit is not designed to distribute profits to owners. Instead, revenue is generally used to support the organization’s mission.

A nonprofit corporation may apply for tax-exempt status if it meets the required rules. Approval depends on how the organization is formed, operated, and maintained.

Nonprofits usually have a board of directors and follow specific reporting and governance requirements.

This structure can be a strong option for founders focused on impact rather than personal profit.

Things to consider

A nonprofit usually needs a board, bylaws, records, state filings, and IRS filings. It may also need state-level charity registration before fundraising. Read What is a Nonprofit | How to Start a Nonprofit.

LLC vs. S Corp vs. C Corp Comparison

The right choice between an LLC, S Corp election, and a C Corporation usually comes down to how much liability protection, tax flexibility, and investor appeal your business needs right now. LLCs offer the simplest setup; the S Corp election can lower self-employment tax once profits grow, and C Corps support larger ownership structures and outside funding.

One of the most common questions entrepreneurs ask is: Should I form an LLC, elect S Corp taxation, or start a C corporation? The table below breaks down how the three options compare.

Factor | LLC | S Corp | C Corp |

Personal Liability Protection | Yes | Yes | Yes |

Tax Flexibility | High | Moderate | Lower |

Ownership Restrictions | Flexible | More restrictions | Most flexible |

Administrative Complexity | Lower | Moderate | Higher |

Investor Appeal | Moderate | Moderate | High |

Best For | Most small businesses | Growing businesses | Investor-backed companies |

Best Business Structure by Business Type

The best business structure depends on what you do, how you earn money, and where you want the business to go. Below are common business types and structures many owners consider.

Freelancers

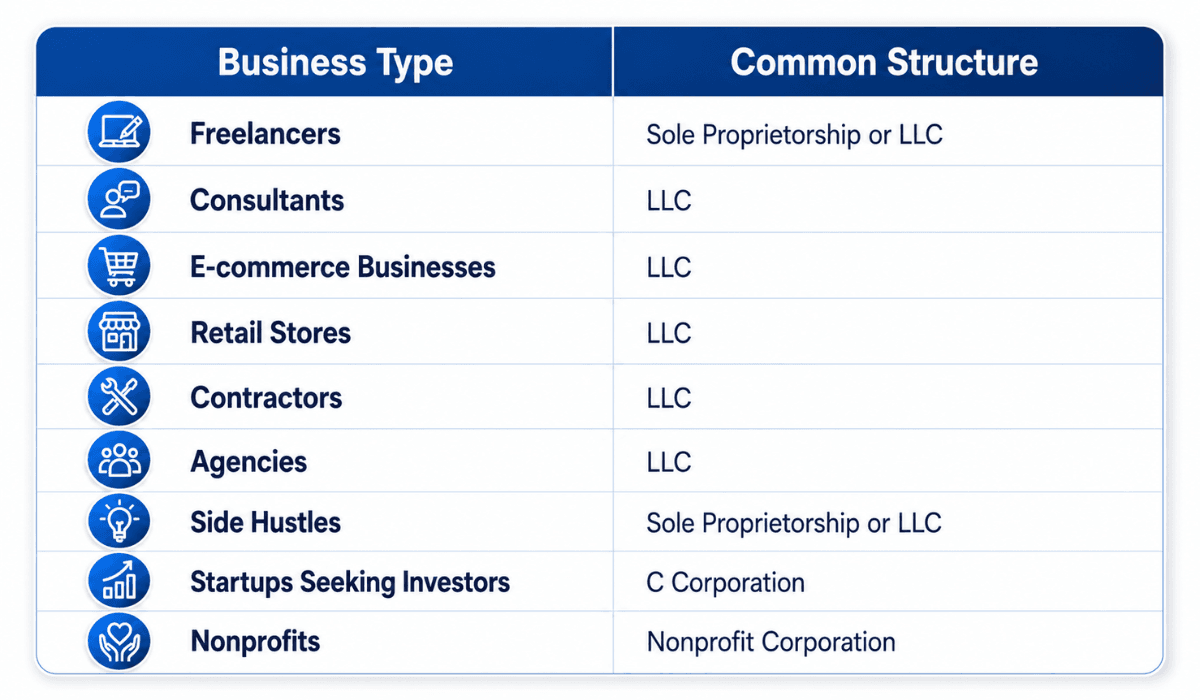

Freelancers (designers, writers, or photographers) often start as sole proprietors because it is simple and low-cost. As their client base grows, many freelancers consider an LLC to create a more formal business structure. An LLC may be worth exploring for freelancers who sign contracts, work with larger clients, or want more separation between personal and business activities.

Consider another option if you plan to bring on partners or raise investment.

Consultants

Consultants often work closely with clients, provide advice, and sign service agreements. Many consultants choose an LLC because it offers flexibility and a professional structure without the complexity of a corporation. Some consultants may later evaluate S Corp taxation if their revenue grows and they meet the requirements.

If your consulting business has steady revenue and you're evaluating tax planning options, it may be worth discussing the S Corp election with a qualified tax professional.

E-commerce Businesses

E-commerce businesses can grow quickly. They may involve online payments, inventory, vendors, customer service, shipping, and returns. Many e-commerce sellers choose an LLC because it can support growth while keeping the structure manageable.

A C Corporation may be worth exploring if you're building a venture-backed e-commerce platform and plan to issue stock.

Retail Stores

Retail stores often work with customers, vendors, employees, inventory, leases, and local business requirements. Because retail businesses usually involve more moving parts than a small side hustle, many owners choose a formal structure early. An LLC is a common option for small retail stores because it offers flexibility and liability protection.

But if you are planning to open multiple locations, bring in investors, or build a larger company with shareholders, a corporation may be worth comparing at that stage.

Contractors

Contractors like landscapers, electricians, and plumbers often work with customers, job sites, vendors, tools, subcontractors, and service agreements. Many contractors consider an LLC because it gives the business a formal structure and can support long-term growth.

However, if you are working with multiple owners or licensed professionals, compare an LLC with a partnership structure, or check whether your state has specific rules for your profession.

Agencies

Agencies often begin with one owner and grow into teams with employees, contractors, clients, and recurring services. An LLC is often a practical option for an agency because it supports flexible ownership and management. As the agency grows, the owner may evaluate tax elections or other structures with a professional.

If your agency plans to raise outside investment, issue stock, or scale into a larger company, a C Corporation may better support those goals.

Side Hustles

Side hustles like selling handmade products, online tutoring, or content creation often start small. A person may sell products online, offer services after work, or test a business idea. A sole proprietorship may be a simple starting point for side hustlers.

As the hustle intensifies, an LLC may be worth considering. If your side hustle starts earning a steady income, involves contracts, or turns into a long-term business, forming an LLC can provide more structure and protection.

Startups Seeking Investors

Startups that plan to raise venture capital or issue stock often have different needs than traditional small businesses. Investors may prefer a C Corporation because it supports stock ownership, future funding rounds, and more complex ownership structures.

But if you are seeking investors and want a simpler structure, an LLC may be a better starting point.

Nonprofits

Mission-driven organizations often choose a nonprofit corporation. This structure is designed for organizations focused on charitable, educational, religious, or community purposes. A nonprofit may later apply for tax-exempt status if it meets the requirements.

A for-profit social enterprise may be a better fit if your goal is to earn profit for owners while pursuing a social mission.

Also read: 35 Best Business Ideas To Start

Can You Change Your Business Structure?

Yes, many businesses change structure as they grow.

A structure that works at the beginning may not be the best fit later. Revenue, risk, partners, employees, funding plans, and tax goals can all change over time.

From Sole Proprietorship to LLC

Many owners begin as sole proprietors and later form an LLC. This can help create a more formal structure as the business grows. The process usually involves choosing a business name, filing LLC formation documents with the state, appointing a registered agent, and meeting state requirements.

From Partnership to LLC

Some partnerships later become LLCs. This can help add structure for ownership, management, and liability protection. Owners may also create an operating agreement to outline how the business will be run.

LLC to S Corp Election

Some LLCs elect S Corp tax treatment after reaching a more stable stage. This does not necessarily change the state-level entity from an LLC. It changes how the business is treated for federal tax purposes if the business qualifies. Business owners often review this option with a business formation specialist.

Final Thoughts

Choosing a business structure is an important step in building a business with confidence. The right structure depends on your goals, ownership setup, tax needs, funding plans, and growth path. Start by understanding your options. Then choose the structure that gives your business the clarity and flexibility it needs for the next stage.

When you're ready to move forward, Swyft Filings can help you form an LLC, corporation, or nonprofit in any state, so you can spend less time on paperwork and more time running your business.

Disclaimer: This article is for general information and isn't legal or tax advice.

Bibliography

[1] SBA. Choose a business structure. Accessed on June 17, 2026

[2] IRS. Limited Liability Company (LLC). Accessed on June 17, 2026

[3] IRS. S corporations. Accessed on June 17, 2026

[4] IRS. Forming a corporation. Accessed on June 17, 2026