LLC, S Corp, or C Corp? Compare taxes, ownership, and compliance side by side, then pick the structure that fits your business. Get started today!

You have an LLC, and your accountant says you should "elect S corp status." Now you are wondering if you have to dissolve your LLC and form something new?

The short answer is: you do not! And this is the most common point of confusion small business owners run into when choosing a business structure.

Here is what most guides miss: an S Corp is not a separate business entity. It is a tax election. Your LLC stays an LLC. You file a form with the IRS that changes how your business is taxed. That is it.

That single misunderstanding trips up thousands of founders every year. This guide breaks down exactly how a C Corp, S Corp, and LLC compare on taxes, ownership, liability, and compliance. By the end, you will know which structure fits where your business is today and where you want it to go.

Key Takeaways

An S Corp is not a business entity. It is a federal tax election that an LLC or C Corp can choose.

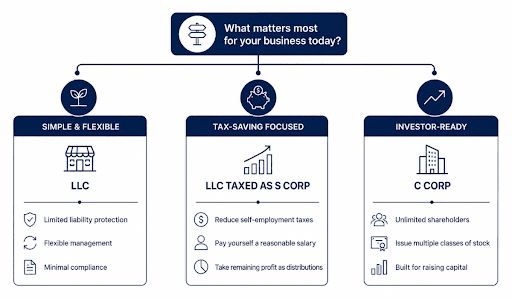

LLCs offer pass-through taxation, limited liability, and the lightest administrative workload.

An S Corp can reduce self-employment taxes for owners earning $60,000 or more in annual net profit.

C Corps are best for startups planning to raise venture capital or issue stock options to employees.

All three structures provide limited liability protection when properly maintained.

Choosing the right structure depends on your current profit level, growth plans, and investor needs.

What Is the Difference Between a C Corp, S Corp, and LLC?

Before comparing them side by side, it helps to understand what each one actually is.

What Is an LLC?

An LLC, or limited liability company, is a legal business structure formed at the state level. It separates your personal assets from your business debts and lawsuits. By default, a single-member LLC is taxed like a sole proprietorship, and a multi-member LLC is taxed like a partnership. Both options send profits straight to your personal tax return, with no separate corporate tax.

LLCs are the most popular business structure in the United States. They combine liability protection with flexible management and minimal paperwork.

What Is a C Corp?

A C Corp is a legal business structure owned by shareholders. It pays its own federal income taxes at a flat 21% corporate rate. If the corporation then distributes profits to shareholders as dividends, those dividends are taxed again on the shareholders' personal returns. This two-layer tax is what people mean by double taxation. [1]

C Corps can have unlimited shareholders, issue multiple classes of stock, and accept investment from foreign nationals and institutions. That is why C Corps are the default structure for startups seeking venture capital.

What Is an S Corp?

An S Corp is a federal tax classification, not a business entity. An existing LLC or C Corp files IRS Form 2553 to elect S Corp status. The legal structure does not change. Only the tax treatment changes.[2]

With S Corp taxation, the business is still a pass-through entity. But the owner must pay themselves a reasonable salary (subject to payroll taxes), and any remaining profit can be taken as a shareholder distribution that is not subject to the 15.3% self-employment tax. That savings is the core reason owners elect S Corp status. [3]

C Corp vs S Corp vs LLC: Full Comparison at a Glance

Here is how all structures compare across the factors that matter most to small business owners.

Feature | LLC | S Corp | C Corp |

Entity Type | Legal structure | Tax election only | Legal structure |

Taxation | Pass-through | Pass-through | Corporate (21% flat rate) |

Double Taxation | No | No | Yes (corporate + dividends) |

Self-Employment Tax | 15.3% on all net profit | 15.3% on salary only | N/A (FICA on W-2 salary) |

Federal Tax Form | Form 1120S [6] | Form 1120 [7] | |

Ownership Limit | Unlimited; foreign OK | Max 100; US citizens /residents only | Unlimited; foreign OK |

Stock Classes | None (membership units) | Single class only | Multiple (preferred + common) |

Compliance Load | Low | Medium | High |

Best For | Small business, flexibility | Profitable owners reducing SE tax | Startups seeking investment |

How Are LLC, C Corp, and S Corp Taxed

Tax treatment is the most important factor in this decision for most small business owners. Here is exactly how each structure works.

How an LLC Is Taxed

By default, an LLC does not file its own federal tax return. Profits flow directly to the owner's personal return.

For a single-member LLC, all profit lands on Schedule C and is treated as self-employment income. The owner pays both the employee and employer sides of payroll taxes, totaling 15.3% on the first $184,500 in net profit and 2.9% on anything above that. [8]

For a multi-member LLC, profits pass through on Schedule K-1 to each partner's personal return. There is no corporate-level tax, which keeps the structure straightforward. [9]

How a C Corp Is Taxed

A C Corp files Form 1120 and pays a flat 21% federal corporate tax on profits.

If the corporation then distributes those after-tax profits to shareholders as dividends, shareholders pay personal income tax on them again. For most shareholders, qualified dividends are taxed at 0%, 15%, or 20%, based on income level.

One important nuance:

If a C Corp reinvests profits back into the business rather than distributing dividends, the second layer of tax is deferred. Many startup founders use this intentionally to grow at the 21% corporate rate before a sale or IPO.

How an S Corp Is Taxed

With S Corp status, business profits still pass through to the owner's personal return, avoiding corporate-level tax.

The key difference from an LLC is the salary requirement. The owner who works in the business must pay themselves a reasonable wage. That salary is subject to payroll taxes. Any remaining profit above the salary can be taken as a shareholder distribution, which is not subject to self-employment tax.

This split between taxable salary and non-SE-taxable distributions is where the savings come from.

S Corp vs LLC: How Much Can You Actually Save on Self-Employment Taxes?

The numbers below show the self-employment tax difference between an LLC and an S Corp at various profit levels, using a $50,000 owner salary as the S Corp baseline.

Annual Net Profit | LLC (SE on all profit) | S Corp (Salary $50K) | Annual Tax Savings |

$60,000 | $8,478 | $7,650 | ~$828 |

$100,000 | $14,130 | $7,650 | ~$6,480 |

$150,000 | $21,194 | $7,650 | ~$13,544 |

$200,000 | $28,234* | $7,650 | ~$20,584 |

*SE tax is calculated as 92.35% of net profit, taxed at 15.3% (12.4% Social Security + 2.9% Medicare).

The Social Security portion is capped at the annual wage base ($184,500 for 2026); Medicare continues uncapped above that threshold. Figures are illustrative. Actual tax owed depends on filing status, deductions, and other income.

Note: These figures represent only the self-employment tax differential. Total tax liability varies by state, deductions, and filing status. Consult a professional before making this election.

What Is the S Corp Reasonable Salary Rule?

The IRS requires S Corp owners who actively work in the business to pay themselves a salary that reflects what someone would earn for doing the same job on the open market. It cannot be zero. It cannot be a token amount.

There is no formula that the IRS publishes. The determination uses a facts-and-circumstances test. Industry wage data, Bureau of Labor Statistics figures, and peer comparisons are all reference points.

The consequences of ignoring this rule are real. In David E. Watson, P.C. v. United States, 668 F.3d 1008 (8th Cir. 2012), a CPA earning substantial revenue paid himself just $24,000 per year. The court recharacterized $67,044 of his distributions as wages, resetting his reasonable salary to $91,044." [10]

When Does an S Corp Election Make Financial Sense?

Most tax professionals use $60,000 in annual net profit as the starting threshold. Below that level, the cost of running payroll, filing quarterly payroll tax returns, and hiring a bookkeeper familiar with S Corp compliance tends to offset the tax savings.

At $80,000 and above, the savings typically exceed the added costs by a meaningful margin. The higher the profit above the reasonable salary amount, the larger the annual savings.

Ownership Rules: LLC vs S Corp vs C Corp

Ownership flexibility varies significantly across the three structures. This matters most when you have multiple founders, outside investors, or international partners.

LLC Ownership

LLCs have no restrictions on who can own them. There is no cap on the number of members. Foreign nationals, other corporations, partnerships, and trusts can all be LLC members. There are no shareholder meeting requirements and no stock to issue. Ownership is tracked through membership units.

S Corp Ownership

S Corps face strict IRS ownership rules:

- Maximum of 100 shareholders

- All shareholders must be U.S. citizens or legal permanent residents

- No foreign nationals or entities as shareholders, with limited exceptions for certain qualified trusts

- Only one class of stock is permitted; all shares must carry equal rights to distributions

These restrictions make S Corp status incompatible with most outside investor arrangements. The moment you accept investment from a VC fund or add a foreign co-founder, S Corp eligibility is gone.

C Corp Ownership

C Corps have no restrictions on ownership. There is no cap on shareholders. Foreign nationals, institutional investors, venture capital funds, and other corporations can all own shares.

C Corps can also issue multiple classes of stock, including preferred shares with special rights, liquidation preferences, and conversion features. This flexibility is why nearly all venture-backed companies operate as C Corps.

Liability Protection: How All Three Compare

All three structures provide limited liability protection when properly maintained. Business owners are generally not responsible (personally) for business debts or legal judgments against the company. Your home, savings, and other personal assets stay separate from business liabilities.

The protection holds as long as you maintain the structure correctly. Courts can set aside liability protection if an owner mixes personal and business finances, fails to keep required records, or uses the entity for improper purposes. Keeping a separate business bank account, maintaining clear records, and following state requirements protect you regardless of which structure you choose.

Compliance Requirements: What Running Each Structure Actually Looks Like

Tax savings and ownership rules are part of the decision. So is the ongoing administrative workload.

Running an LLC

LLCs carry the lightest compliance load of the three. There are no required annual shareholder meetings, no mandatory board of directors, and no required officer roles. Management structure is defined by your operating agreement, which you control.

Ongoing requirements typically include filing an annual state report, maintaining a registered agent, and keeping business and personal finances separate. Most single-member LLC owners manage these tasks without outside help.

Running an S Corp

Electing S Corp status adds compliance requirements. You will need to run payroll, withhold and remit payroll taxes quarterly, and file Form 1120S at year-end, plus issue Schedule K-1s to all shareholders.

You also need to maintain corporate formalities: a board of directors, officer roles, bylaws, and records of major business decisions. Annual additional cost for accounting and payroll services typically ranges from $ 1,500 to $2,500, depending on the complexity of your situation. This cost should factor into whether the election saves more than it costs for your specific profit level.

Running a C Corp

C Corps carry the most requirements. Annual shareholder meetings, board of directors meetings, formal minutes, detailed corporate records, and Form 1120 filings are all required. Delaware C Corps also owe an annual Delaware franchise tax based on either authorized shares or assumed par value.

These requirements take time and money. But they also create the organizational transparency that investors rely on during due diligence. The compliance infrastructure a C Corp builds early tends to make raising capital smoother later.

Why Startups and Investors Choose the C Corp

Venture capital firms overwhelmingly require C Corp status before they'll invest. The reason is structural, not arbitrary.

Venture capital funds invest through preferred stock, which requires multiple stock classes. Only a C Corp can issue preferred stock. S Corps cannot. LLCs can create economically similar arrangements, but most institutional investors will not accept them.

Also, there is a tax issue for institutional investors such as university endowments or pension funds. These entities face restrictions on receiving pass-through income from partnerships and S Corporations. A C Corp eliminates that problem. The investor receives dividends or capital gains, not a K-1 with phantom income that they did not receive as cash.

The Delaware C Corp Advantage

Most venture-backed companies incorporate as Delaware C Corps even when they operate in a different state. Delaware has the most developed body of corporate case law in the country, a specialized Court of Chancery for business disputes, and governance rules that investors know well.

Many term sheets specify a Delaware C Corp as a requirement before investment closes. Incorporating in Delaware means registering as a foreign entity in your home state, which adds a filing fee but is a straightforward process.

Stock Options and Employee Equity

C Corps can issue Incentive Stock Options (ISOs) to employees, which receive favorable long-term capital gains treatment for the recipient. This is the standard equity compensation tool for high-growth companies.

S Corps and LLCs cannot easily replicate this structure. That limitation matters if you plan to attract talent with equity as part of the compensation package.

Which Business Structure Is Right for You?

There is no single best structure. The right choice depends on where your business is today and where you are taking it.

Choose an LLC If

- You are a freelancer, consultant, or early-stage service business

- Your annual net profit is currently below $60,000

- You want minimal paperwork and administrative overhead

- You hold real estate assets and want clean liability separation

- You have or expect foreign partners or investors

- You want to test a business concept before committing to a more formal structure.

Choose a C Corp If

- You plan to raise venture capital (VC) or angel funding

- You want to issue stock options to retain employees

- You are building toward an acquisition or public offering

- You have or expect foreign shareholders or institutional investors

- You want to reinvest profits into the business at the 21% corporate rate before a liquidity event

The table below matches common business types to the structure that fits them best.

Business Type | Best Starting Structure |

Freelancer or solo consultant | LLC |

Service business at $60K+ net profit | LLC taxed as S Corp |

Real estate holdings | LLC (one per property recommended) |

High-revenue professional (doctor, lawyer, CPA) | S Corp |

Tech startup seeking venture capital | Delaware C Corp |

Small retail or restaurant | LLC |

Multi-founder company seeking institutional investment | Delaware C Corp |

In the End

None of the business structure choices are permanent. You can start as an LLC, elect S Corp status when profit justifies it, and convert to a C Corp if you raise institutional funding down the road. The structure that fits today doesn't have to be the one you keep forever.

Swyft Filings handles the paperwork for all three. Whichever direction fits your business, we'll do the paperwork so you can focus on running it.

Bibliography

[1] Internal Revenue Service. Publication 542, Corporations. Accessed on July 7, 2026

[2] Internal Revenue Service. About Form 2553, Election by a Small Business Corporation. Accessed on July 7, 2026

[3] Internal Revenue Service. Self-Employment Tax (Social Security and Medicare Taxes). Accessed on July 7, 2026

[4] Internal Revenue Service. About Schedule C (Form 1040). Accessed on July 7, 2026

[5] Internal Revenue Service. About Form 1065, U.S. Return of Partnership Income. Accessed on July 7, 2026.

[6] Internal Revenue Service. About Form 1120-S, U.S. Income Tax Return for an S Corporation. Accessed on July 7, 2026.

[7] Internal Revenue Service. About Form 1120, U.S. Corporation Income Tax Return. Accessed on July 7, 2026.

[8] Social Security Administration. Contribution and Benefit Base. Accessed on July 7, 2026.

[9] Internal Revenue Service. About Schedule K-1 (Form 1065). Accessed on July 7, 2026.

[10] Internal Revenue Service. S Corporation Employees, Shareholders, and Corporate Officers. Accessed on July 7, 2026.