An LLC is a state-registered business structure providing a legal identity, asset protection, and pass-through taxation to keep your personal and business finances separate.

It is a limited liability company in simple terms. But knowing this definition of LLC is not enough, right?

This does not tell you how to run one, how to keep it protected, or how to avoid the mistakes that quietly undo the protection you paid for.

Nearly 503,171 new business applications were filed in the U.S. in April 2026 alone. [1]

Most of those founders probably had the same questions you do right now.

- How much does it cost to start an LLC?

- How is a limited liability company taxed?

- What's the downside of having an LLC?

We’ve answered all these questions and many others for you in this guide. Keep reading to know more.

What This Guide Covers

How an LLC is structured and governed, and about its members, managers, and operating agreements

Every tax classification an LLC can use, including S Corp and C Corp elections.

The exact steps to form an LLC correctly from day one

What compliance looks like after formation, including reports, fees, licenses, and recordkeeping

Where liability protection holds and exactly where it breaks down

How to handle ownership changes, member exits, and dissolution

The most common LLC mistakes and how to avoid all of them

What Does LLC Stand For?

LLC stands for Limited Liability Company. Each word has a specific legal meaning.

Limited means your personal financial exposure is capped if your business owes money or faces a lawsuit; your personal assets are generally not at risk.

Liability refers to legal responsibility. Without an LLC, you and your business are the same legal person. Every business debt or lawsuit touches you directly.

Company means this is a formally recognized entity registered with your state. It has its own legal identity, separate from you as an individual.

The U.S. Small Business Administration describes the LLC as a structure that combines corporation-style protection with partnership-style flexibility on taxes.

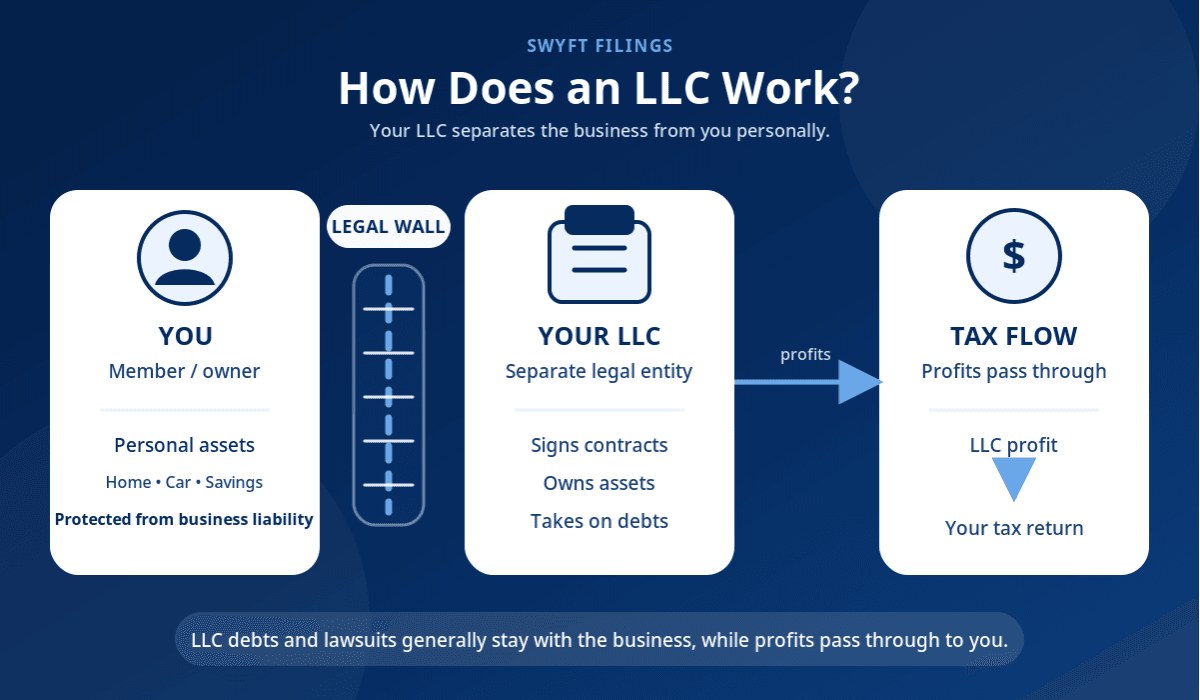

How Does An LLC Work?

An LLC works by creating a legal wall between you and your business. Think of it as a separate person. It owns its assets, signs its own contracts, and assumes its own debts.

You create that wall by filing a document called Articles of Organization with your state's Secretary of State. That filing makes your LLC official. From that point forward, the business exists as a separate legal entity.

Here is a practical example:

Say you run a catering LLC. A client claims your food caused an allergic reaction and sues for $200,000. Because your business is an LLC, the lawsuit targets the business, not you. The court cannot reach your personal savings, car, or home, as long as you have kept your personal and business finances separate.

That legal separation is called the corporate veil. It is the foundation of LLC protection.

⚠️ Important: LLC protection is not absolute. If you mix personal and business funds, a court can pierce the corporate veil and hold you personally responsible. Always maintain a separate business bank account.

Read our What Is A Limited Liability Company (LLC)? blog for more details!

LLC Ownership: Members, Managers, And Operating Agreements

Who Are "Members"?

The owners of an LLC are called members. You can have one member or many. Most states place no limit on who can hold membership. Individuals, corporations, other LLCs, and even foreign nationals can all be members of a U.S. LLC.

Member-Managed Vs. Manager-Managed

You choose how your LLC is run.

In a member-managed LLC, the owners handle day-to-day decisions. This is the most common setup for small businesses.

In a manager-managed LLC, members appoint a manager (who may or may not be a member) to run operations. This works well when some members are passive investors who want no role in daily decisions.

What Is An Operating Agreement?

An operating agreement is an internal document that defines how your LLC runs. Most states do not require you to file it publicly, but every LLC should have one.

It covers:

- How profits and losses are split among members

- Who has voting rights and on what decisions

- What happens when a member wants to leave or transfer ownership

- How new members can be added

- What steps should the LLC follow if it needs to dissolve

Without an operating agreement, your state's default rules govern these situations. Those defaults rarely match what you actually want. Writing one before you start operating is one of the most important steps you can take.

Section | What It Covers |

General Business Information | LLC name, address, duration, purpose |

Management Structure | Member-managed vs. manager-managed, signing authority |

Tax Designation | How the LLC is taxed (partnership, S Corp, C Corp) |

Member Information | Names, ownership percentages, capital contributions |

Decision-Making | Voting thresholds for major business decisions |

Membership Changes | Buy-sell provisions: What happens if a member exits |

LLC Dissolution | Process for winding down, settling debts, and distributing assets |

What Are The Benefits Of Forming An LLC

Personal Asset Protection

Your home, savings, and personal property are off-limits in a business lawsuit, as long as you keep business and personal finances separate. This protection is ongoing from the day you start an LLC.

Pass-Through Taxation by Default

The IRS does not tax the LLC itself. Profits flow directly to members' personal tax returns. You pay taxes once, not twice, like a C Corporation, where profits get taxed at the corporate level first and again when distributed to shareholders.

Tax Election Flexibility

You can elect S Corp tax status by filing IRS Form 2553. This lets you pay yourself a reasonable salary (subject to payroll taxes) and take the remaining profit as distributions, which are not subject to self-employment tax. For LLC owners earning more than $60,000 in net profit per year, this election can save thousands of dollars annually.

Business Credibility and Banking Access

Adding "LLC" to your name signals that your business is formally registered. Banks, vendors, and clients take registered entities more seriously. It also makes it easier to open a business bank account and build a separate business credit profile.

Flexible Profit Distribution

An operating agreement can set profit splits differently from ownership percentages. Members can draw income in ways that match their contributions, not just their ownership stake.

Business Name Protection

Your LLC name is officially registered in your state. No other LLC in that state can use the same name.

What Are The Disadvantages Of An LLC

Self-employment Tax

Profits pass through to you as self-employment income. You pay the full 15.3% self-employment tax, covering Social Security (12.4%) and Medicare (2.9%). [2] Employees pay only half because employers cover the other half. You can deduct half of this tax from your taxable income.

State Fees Add Up

Filing fees range from $35 to $500, with a national average of about $132. Many states also charge annual report fees. California requires an $800 annual franchise tax regardless of whether the LLC earns any income.

Compliance Obligations Still Exist

LLCs need to file annual or biennial reports, pay state fees, and maintain a registered agent address. These are simpler than corporate requirements, but missing them can result in your LLC losing good standing.

Harder To Raise Venture Capital

Venture capitalists typically fund C Corporations because they can issue stock. LLCs cannot issue shares, which makes them less attractive for large-scale VC funding or IPOs.

Member Transitions Can Be Complicated

If a partner leaves or passes away, some states may require the LLC to be dissolved and reformed unless your operating agreement addresses those scenarios in advance.

What Are The Types Of LLCs?

Single-Member LLC

One owner holds 100% of the membership. The IRS treats it as a disregarded entity, meaning income flows directly to your personal tax return on Schedule C. This is the simplest structure for solo business owners.

Multi-Member LLC

Two or more people own the business. The IRS treats a multi-member LLC as a partnership by default. The LLC files Form 1065 and issues each member a Schedule K-1 showing their share of income or loss.

Domestic LLC

It is an LLC formed and operating in the same state. Most small businesses start as domestic LLCs in their home state.

Foreign LLC

If you formed an LLC in one state but operate in another, you register as a foreign LLC in that second state. This is called a foreign qualification and involves a registration process with that state's Secretary of State.

Professional LLC (PLLC)

Certain licensed professionals, such as doctors, lawyers, and accountants, may be required to form a PLLC instead of a standard LLC. Rules vary by state, and licensed professionals often remain personally liable for their own malpractice even inside a PLLC.

Series LLC

A Series LLC acts as a master entity that allows separate "series" to exist under it, each with its own assets and liability protection. This structure is popular among real estate investors who want to hold multiple properties, with each property isolated from risk.

Also Read: What Are the Different Types of LLCs? To know the types in detail!

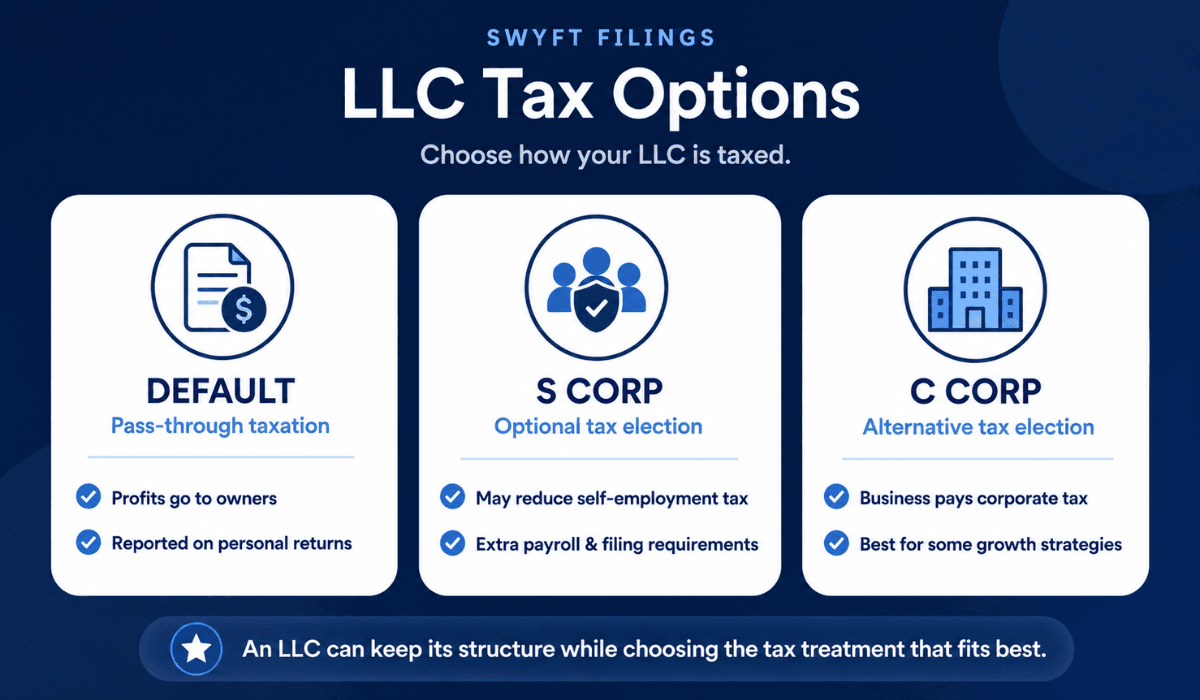

How Is An LLC Taxed?

Default: Pass-Through Taxation

By default, the IRS does not tax an LLC as a separate entity. Profits and losses pass through to members and are reported on personal tax returns.

A single-member LLC is treated as a disregarded entity. All income flows to Schedule C on your personal Form 1040.

A multi-member LLC is treated as a partnership. The LLC files Form 1065, and each member receives a Schedule K-1.

Self-Employment Tax

LLC members who actively work in the business pay self-employment tax on their share of profits. The 2026 rate is 15.3%, covering Social Security (12.4%) and Medicare (2.9%). You can deduct half of this tax from your personal taxable income.

S Corp Tax Election

If your net profit consistently exceeds $60,000 per year, electing S Corp status can reduce your self-employment tax burden. You pay yourself a reasonable salary (subject to payroll taxes) and take remaining profits as distributions, which are not subject to the 15.3% self-employment tax.

This election is made by filing IRS Form 2553. The LLC keeps its legal structure. Only the tax treatment changes.

C Corp Tax Election

If you plan to reinvest profits heavily into the business, C Corp tax treatment may make sense. Corporate profits are taxed at a flat 21% federal rate. This can be beneficial at higher income levels, but it introduces double taxation when profits are eventually distributed to members.

You can elect C Corp tax treatment by filing IRS Form 8832.

LLC Tax Treatment Summary

Tax Treatment | Default? | Best For |

Disregarded entity (sole proprietor) | Yes (single-member) | Simple, lower-income operations |

Partnership | Yes (multi-member) | Multiple owners with shared income |

S Corp election | Optional | Profitable LLCs above $60K net profit |

C Corp election | Optional | Businesses reinvesting profits heavily |

How To Start An LLC: Step-By-Step?

Step 1: Choose Your Business Name

Your name must be unique in your state and include a legal designator like "LLC," "L.L.C.," or "Limited Liability Company." Check your state's business name database or a name availability checking tool before filing to confirm availability.

Step 2: Select Your Formation State

Most owners form an LLC in the state where they live and operate. Filing in Delaware or Wyoming for tax advantages only makes sense if you have specific legal or financial reasons for doing so. For most small business owners, the home state is the practical and correct choice.

Step 3: Appoint A Registered Agent

Every state requires you to designate a registered agent with a physical address in that state. This person or company receives legal documents and official state notices on behalf of your LLC. You can serve as your own registered agent, or you can use a professional registered agent service to keep your personal address off the public record.

Step 4: File Your Articles Of Organization

This is the official document that creates your LLC. You file it with your state's Secretary of State and pay the required state filing fee. The filing process can be started easily through a formation service.

Step 5: Create An Operating Agreement

Write an operating agreement before your limited liability company starts doing business. Outline how the LLC is managed, how profits are split, and what happens if a member leaves. Most states do not require you to file it publicly, but it is the most important internal document your LLC will have.

Step 6: Get An Employer Identification Number (EIN)

An EIN is your business's federal tax ID. You need it to open a business bank account, hire employees, file federal taxes, and register for state tax accounts. Apply directly through the IRS website for free. [3]

Step 7: Open A Business Bank Account

A separate business bank account is essential. It keeps your personal and business finances apart, which protects your corporate veil. Mixing funds is one of the most common reasons courts pierce that protection.

Step 8: Register For State Taxes And Licenses

Depending on your state and business type, you may need to register for state sales tax, payroll taxes, or a business license. Check your state's requirements before you start operating.

Check the detailed guide on starting an LLC here!

How to Keep An LLC Compliant After Formation?

Forming a limited liability company is not a one-time task. Staying in good standing requires ongoing attention.

Annual Or Biennial Reports

Most states require LLCs to file an annual or biennial report confirming the LLC's active status and current information. Missing the deadline can result in your LLC losing good standing or being administratively dissolved.

Franchise Taxes

Some states charge a franchise tax on LLCs regardless of income. California charges $800 per year. Other states calculate this based on revenue or members. Research your state's requirements before filing.

Registered Agent Maintenance

Your registered agent information must stay current. If your agent's address changes or the agent resigns, you must update your state records promptly. Failing to maintain an active registered agent can affect your business standing.

Licenses And Permits

Your LLC may need a local business license, a state professional license, or an industry-specific permit. These requirements vary by location and business type. Confirm what applies before you start operating.

Recordkeeping And Bookkeeping

Keep clean, separate records for your business. Track income, expenses, and distributions accurately. These records protect you if your LLC is ever audited and support the legal separation between you and your business.

Keeping Finances Separate

Never mix personal and business funds. Commingling is the single most common reason courts hold LLC members personally liable. Maintain a dedicated business bank account and business credit card from day one.

Also read: 15 Common LLC Mistakes to Avoid in 2026!

LLC Legal Protection: What It Covers and What It Does Not?

What LLC Protection Covers

- Business debts your company cannot repay

- Lawsuits from clients, customers, or third parties against the business

- Claims arising from business contracts or services provided under the LLC

When LLC Protection Does NOT Apply?

Fraud or illegal acts:

If you use the LLC to commit fraud or engage in illegal activity, courts will pierce the corporate veil and hold you personally liable.

Personal guarantees:

If you personally sign for a business loan or lease, you are personally liable for that obligation regardless of your limited liability company status.

Commingling funds:

Mixing personal and business money destroys the legal separation your LLC creates. Courts can hold you personally responsible if this happens.

Professional malpractice:

In many states, licensed professionals remain personally liable for their own malpractice, even inside a PLLC.

Unpaid payroll taxes:

The IRS can pursue personal liability for trust fund taxes in certain situations, even when business assets are held in an LLC.

LLC vs. Other Business Structures

How Does LLC vs. Sole Proprietorship Compare?

Feature

Sole Proprietorship

LLC

Personal liability

Full personal liability

Personal assets protected

Setup cost

Free or very low

$35 to $500 in state fees

Taxes

Pass-through

Pass-through

Business credit

Hard to build

Can build separately

Credibility

Informal

Formally registered

As a sole proprietor, a single lawsuit can reach your personal savings. As an LLC member, the business absorbs the hit. That difference matters most once you start earning a consistent income or taking on real business risk.

Also read: What is a Sole Proprietorship for more information!

How Does An LLC Vs. A Corporation Vs. An S Corp Compare?

Feature | LLC | S Corp | C Corp |

Liability Protection | Personal assets protected | Personal assets protected | Personal assets protected |

Taxation | Pass-through (Taxed once) | Pass-through (Taxed once) | Double Taxation (Corporate + Individual) |

Self-Employment Tax | Paid on all profits | Paid on salary only | Not applicable |

Ownership Limits | Unlimited members | Max 100 (US citizens only) | Unlimited |

Management | Flexible; minimal rules | Formal; board & meetings | Strict; board, officers, & meetings |

How Does LLC Vs. Partnership Differ?

In a general partnership, every partner is personally responsible for the business's debts and for each other's actions. An LLC eliminates that personal exposure by creating a separate legal entity. You get the flexibility of a partnership with the liability shield of a corporation.

When Does Each Structure Make Sense?

- Sole proprietorship: You are testing an idea and have minimal risk exposure.

- LLC: You are running an active business with any meaningful financial or legal risk.

- S Corporation: Your net profit exceeds $60,000, and you want to reduce self-employment taxes.

- C Corporation: You plan to raise venture capital, issue stock, or take the company public.

Who Should Form an LLC?

Should Freelancers And Consultants Form An LLC?

Yes, a limited liability company is where a lot of freelancers start. One unhappy client can sue for damages. An LLC keeps that lawsuit away from your personal savings. It also signals professionalism to clients who prefer contracting with a registered business entity.

Is LLC The Right Business Structure For E-Commerce Sellers?

Yes. Defective products, shipping disputes, chargebacks, and customer claims are real risks for online sellers. An LLC draws a line between your store's problems and your personal finances. It also helps with opening a merchant account and building business credit.

Should Real Estate Investors Form An LLC?

Yes. A Series LLC is especially useful here. You can place each property in its own series, so a problem with one does not drag the others into a lawsuit. LLCs also make it easier to transfer property ownership and finance future purchases under a separate business credit profile.

Do Small Business Owners With Employees Need Limited Liability?

Yes, when you start hiring employees, protecting your personal assets becomes even more important. A limited liability company creates a clear legal structure for employment agreements and business liability.

When Should Side Hustlers Form An LLC?

Once you start earning a consistent income, the risk profile of your work changes. Formalizing as an LLC is a practical, low-cost step toward treating your side business like a real one.

Ownership Changes, Transfers, and Dissolution

How Do I Add A New Member To My LLC?

Adding a member typically requires an amendment to your operating agreement and, in some states, an update to your state filing. Your operating agreement should outline the process for admitting new members and set any approval requirements.

How Do I Remove Or Buy Out A Member?

Your operating agreement's buy-sell provisions govern this. A well-written buy-sell clause sets a valuation method, a payment timeline, and conditions under which a buyout can be triggered, including voluntary departure, disability, or death.

How Is LLC Ownership Transferred?

Ownership interests in a limited liability company are called membership interests. Transferring them requires following the procedure in your operating agreement. Most operating agreements require the remaining members to approve any transfer to a third party.

What Happens To The LLC If A Member Dies?

Without operating agreement provisions addressing this, the deceased member's interest may pass to their heirs, who could then have a claim on the business. A properly drafted operating agreement should include a clause that allows remaining members to buy out a deceased member's interest.

How Do I Properly Dissolve An LLC?

To dissolve a limited liability company, you typically:

- Follow the dissolution procedures in your operating agreement.

- Settle all outstanding business debts and obligations.

- Distribute remaining assets to members based on ownership percentages.

- File Articles of Dissolution with your state's Secretary of State.

- Close your business bank accounts and cancel licenses or permits.

Can I Convert My LLC To Another Entity Type?

You can convert a limited liability company to a corporation, or vice versa, if your business needs change. This is common when a growing company needs to raise venture capital and switches from an LLC to a C Corporation. The process varies by state and usually involves filing conversion paperwork with the Secretary of State and updating your IRS tax classification.

What Are The Common LLC Mistakes To Avoid?

Mixing personal and business money:

This is the most common and most damaging mistake. It can eliminate your liability protection entirely. Open a business bank account before you start operating.

Skipping the operating agreement:

Without one, your state's default rules govern your LLC. Those defaults often do not match how you actually want to run your business or handle ownership disputes.

Forgetting annual filings:

Most states require annual or biennial reports. Missing these deadlines can result in fines, loss of good standing, or administrative dissolution of your LLC.

Choosing the wrong state:

Filing in Delaware or Wyoming when you operate in another state usually creates more administrative work, not less. You may need to register as a foreign LLC in your home state anyway. For most small businesses, forming in the home state is the right move.

Using the LLC before it is officially formed:

Contracts and transactions made before your LLC is officially registered do not carry the protection of the LLC structure. Wait until your Articles of Organization are accepted by the state before transacting under the LLC name.

Ignoring tax deadlines:

LLC members pay estimated quarterly taxes on their share of profits. Missing these payments can result in IRS penalties. Set up a tax calendar after formation.

Not updating the operating agreement:

When members join, leave, or the business changes significantly, your operating agreement should be updated to reflect the new reality.

What Are The Common Misconceptions About LLC’s?

"An LLC means I pay no taxes."

This is False! The LLC itself does not pay federal income tax by default, but you, as the member, still pay taxes on your share of profits through your personal return. Forming an LLC does not lower your tax rate.

"An LLC is the same as a corporation."

False. An LLC and a corporation are different legal structures with different management requirements, tax treatments, and compliance obligations.

"An LLC protects me from all lawsuits."

False. The protection covers business-related claims when proper separation is maintained. Personal malpractice, fraud, commingling funds, or personal guarantees can all break through that protection.

"An LLC is expensive to maintain."

It depends on your state. Some states charge minimal annual fees. Others, like California, charge $800 per year regardless of income. Research your state's specific requirements before forming.

"I need a lawyer to form an LLC."

Not true. Most entrepreneurs form an LLC by filing Articles of Organization directly with their Secretary of State, or through a business formation service. You do not need a lawyer to complete the paperwork.

Takeaway

We’ve covered everything from formation and tax elections to compliance and ownership changes to help you start your LLC with confidence. If you have any remaining questions or need expert guidance on your specific state’s requirements, our specialists are here to help. Reach out via phone or live chat today.

Bibliography

- U.S. Census Bureau. Business Formation Statistics, April 2026. Accessed on May 15, 2026.

- Internal Revenue Service. Self-Employment Tax (Social Security and Medicare Taxes). Accessed on May 15, 2026.

- IRS. Apply for an EIN Online. Accessed on May 15, 2026.