Selling an S corp is a complicated process, but there are strategies to minimize your taxes on capital gains and goodwill during the sale of the business.

If you’ve decided to sell your S corp, it’s crucial to conduct the sale of the business in a manner that rewards you financially.

The tax implications of selling an S corp can be significant. Understanding the taxes on the sale of a business held in an S corp can help you structure the transaction in a way that reduces surprises at closing and on your tax return. This guide walks you through selling a business to minimize or defer some of these taxes.

Key Takeaways

Selling an S Corp is complicated, but you may experience significant tax savings by making informed decisions when structuring the S corp sale.

To sell an S corp, you must determine the value of the business, choose a selling method (Asset, Stock, or 338(h)(10) election), and finalize contracts.

Goodwill, or the intangible assets of your business, can significantly affect tax treatment with the sale of an S corp.

Active shareholders who materially participate in the business may be exempt from the 3.8% NIIT on their sale proceeds, though certain asset-level nuances apply in asset sales.

Before You Sell: Due Diligence Checklist

- Verify the S-Election: Make sure your Form 2553 was filed correctly. Many S-elections are technically invalid due to filing errors.

- Clean up the Cap Table: Confirm all share ownership documentation is current, especially if exiting an S corp with multiple minority shareholders.

- Check Debt Obligations: Determine what happens to S Corp debt when the company is sold. Will the buyer assume it, or must it be paid off at closing?

- Tax Nexus Review: Resolve any state tax issues related to remote employees or economic nexus before a buyer’s due diligence team flags them.

How to Sell an S Corp

Selling an S Corp can be a complicated process, and there are various methods for doing so. The following outlines everything you need to know about selling this business type.

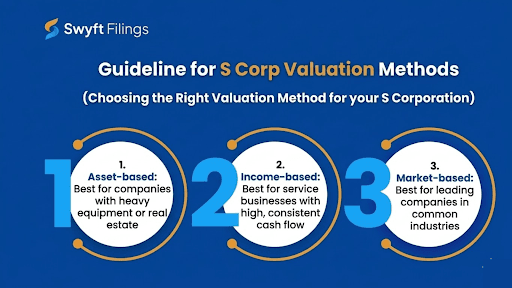

1. Determine the Value of the S Corp

Your first step in the sale of a business is determining the fair market value. There are three main methods of valuing an S Corp, each with advantages and disadvantages.

Given the tax implications of selling a business, choosing the ideal valuation method for your situation is essential. A CPA can help review tax laws, assess the value of your S corp, and determine the best valuation method.

Asset-based valuation

Asset-based valuation determines the fair market value of the business’s assets. This process involves calculating the combined value of all tangible and intangible assets and deducting liabilities. The result is the fair market value of the business.

Asset-based valuation is ideal for companies with significant business assets. Tangible capital assets include property, equipment, and investments like stocks, bonds, and options. Intangible assets include intellectual property, trademarks, and branding.

Income-based valuation

Income-based valuation uses the S corporation’s cash flow, profitability, and revenue to determine company value. The value is determined based on past, current, or expected future cash flows.

Income-based valuation is best for companies that have experienced a healthy revenue stream and consistent cash flow. If sales have been low or inconsistent, consider another valuation method.

Market-based valuation

With a market-based valuation, your company's worth is compared to similar businesses in your industry. This method analyzes earnings, revenue, and assets to consider the current market prices of comparable companies that have recently sold or are available for sale.

The market-based valuation method uses price-related indicators, including sales and book values. Book values refer to what the S corporation shareholders would receive if the company were to undergo liquidation.

The market-based valuation method is best for leading companies in their industry.

2. Choose a Selling Method

Once you determine the fair market value for your business, you are ready to choose a sales method. We’ll dive into each below.

Sale of Stock

In a stock sale, the buyer purchases the S Corp stock, taking on all the assets and liabilities of the company. This is often preferred by sellers because it typically results in a single level of taxation at the long-term capital gains rate. With this process, the ownership of the stock changes, but the company essentially remains the same.

A sale of S corporation stock to another shareholder is generally treated as a stock sale, with gain or loss measured against the seller’s stock basis.

Here are the steps to a stock sale for a company with Subchapter S status:

- Prepare and execute a contract outlining the terms for a sale of stock between you and the buyer.

- Outline a stock transfer agreement that contains the names of the current owners of shares and the buyers, the number of shares being transferred, and the amount paid for the shares.

- Sign the stock transfer agreement as the seller to execute the sale.

- Record the S corporation stock sale and revise the stock ledger to reflect the new ownership.

- Distribute Schedule K-1s to new and former shareholders to report share of income.[1]

- Finalize the sale with a Schedule D (1040) tax form to report any stock gains or losses.[2]

Sellers are subject to capital gains tax if there is a long-term capital gain on the stock. If the stock is worth more at the time of sale than when you bought it, you must pay capital gains tax.

To calculate your capital gains, you subtract your tax basis, or how much you originally spent on the stock, from the stock’s current worth. If there is a gain, you owe tax on that amount, minus any transaction costs from the sale.

Knowing how to calculate stock basis for an S corp is critical because basis affects both gain on sale and whether some distributions are taxable.

Sale of Assets

In an asset sale, the buyer purchases all your company assets and forms a new company. Some assets are capital assets and may receive favorable capital gains tax treatment.

Long-term capital gains, consisting of assets owned for a year or more, are taxed significantly lower than ordinary income.

On the other hand, assets added back to prior depreciation will be taxed at ordinary income tax rates. This is known as depreciation recapture and is calculated by comparing the adjusted cost basis of the asset with the sale price. When an asset is sold for more than its market value but less than its initial purchase price, it’s treated as ordinary income and taxed accordingly.

Steps to Completing an Asset Sale:

The asset sale process can be complicated and involves several steps. Each asset sold is treated separately for partnerships, LLCs, and sole proprietors. Here’s a breakdown of the steps in this process:

- Assign a tax basis to each asset: Take the asset’s original purchase price and add or subtract changes from the initial value. If the asset doesn’t have a tax basis, then it is subject to income tax rates.

- Allocate a purchase price for each asset: Generally, the purchase price of each asset is determined based on fair market value. You must categorize assets into the seven IRS classes (Cash, Securities, Receivables, Inventory, Tangible Property, Intangibles/Section 197, and Goodwill). Some sellers find that getting a third-party appraisal helps with a more accurate allocation of purchase prices.

- Coordinate IRS Form 8594: Both the buyer and seller must file this form with their tax returns. It is critical that the allocation numbers on the buyer's form match the seller's form to avoid an IRS audit.

- Determine Tax Liability: Calculate how much capital gains will need to be paid (on assets like goodwill) versus income tax (on inventory and depreciation recapture) if you, as the seller, receive a profit from selling the business.

Section 338(h)(10) Election:

A Section 338(h)(10) election can give buyers and sellers the best of both worlds. Legally, the deal remains a stock sale, so ownership transfers without retitling every individual asset.

For tax purposes, though, the transaction is treated like an asset sale, which lets the buyer step up the basis of the company’s assets.

Important: This is a bilateral election. To execute it, both parties must sign and file IRS Form 8023. Subsequently, both the buyer and seller must attach Form 8883 to their respective tax returns to report the asset allocation. [3] [4]

Installment Sale

If the sale of your business is financed and you receive at least one payment after the tax year of the sale, you can consider making an installment sale. This allows you to defer some of the tax due on capital gains until you receive payment in future years. Only income from capital gains can qualify for installment sale treatment.

According to the IRS, under the installment method, you “include in income each year only the part of the gain you receive or are considered to have received.”[5] The U.S. Small Business Association (SBA) states that you aren’t able to use installment sale reporting for the sale of inventory or receivables.[6]

Factor | S Corp Sale | LLC Sale |

Tax treatment | Pass-through; capital gains at the shareholder level | Pass-through; membership interests differ |

Stock sale option | Yes, shares of stock | No stock; membership transfer |

Built-in gains tax | Possible if prior C corp | Not applicable |

Self-employment tax | Not applicable. Proceeds from stock or asset sales are not considered SE income. | Generally not applicable. Gain from the sale of partnership interests or capital assets is excluded from SE tax. |

3. Finalize Contracts and Negotiations

The final step in the S Corp sales process is the purchase agreement. This must be carefully structured and outlined to protect the owner’s interests.

The agreement should include the buyer and seller information, outline the terms and conditions of the sale, and specify the obligations and rights of the seller and buyer.

The purchase agreement must also contain the purchase price, selling method, sale inclusions and exclusions, important disclosures, payment terms, and any contingencies, such as if there will be an installment sale.

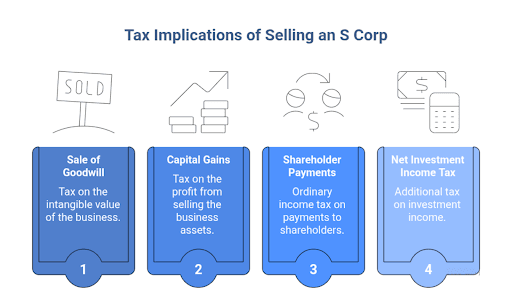

Tax Implications of Selling an S Corp

Depending on how you set up the sale of your S corp, you can face significant taxes on the sale of the business. With careful tax liability planning, you can minimize or defer some of the taxes you owe the IRS.

Familiarize yourself with the following tax situations and learn how you can maximize tax benefits during the sale of a business.

Sale of Goodwill

One aspect that affects tax treatment with the sale of an S Corp is what is known as goodwill. Generally, goodwill represents the intangible assets that keep customers returning to use your services.

In the sale of an S corporation, goodwill is the amount paid above and beyond the fair market value of the company’s assets. With most businesses, there is value beyond the physical business assets. These intangible assets are often the reason why someone buys a business rather than starts a new one.

Intangible assets are built up over time. Examples of goodwill include the following:

- Brand reputation: How well-known your brand is and the positive associations customers have with it.

- Reputation for quality workmanship: The level of trust and satisfaction your company has earned in the market.

- Company prestige: The overall status and distinction of your business in its industry.

- Intellectual property: This can include patents, trademarks, and copyrights that belong to the business.

- Employee relations: The value of having a skilled, happy, and well-managed workforce.

- Loyal customer base: Regular customers who consistently choose your services over competitors.

- Robust earning capacity: A demonstrated ability to generate consistent and strong profits.

- Well-known and respected business name: The inherent value in your company’s trade name.

How to Calculate Goodwill?

Goodwill is derived once all assets have been allocated. It is calculated by taking the company purchase price and subtracting the difference between the value of the liabilities and assets and the fair market value. The sale of goodwill represents the amount that is left over.

Regarding goodwill tax, these intangible assets are considered capital gains and are generally taxed as capital assets.

Some goodwill is considered “going-concern value.” This refers to the value of a business continuously operating successfully and aligned with its intended purpose after its sale. Going-concern value is usually not subject to allocation for tax purposes.

Capital Gains Taxes

Capital gains taxes are taxes paid on the profits you make from selling your business. A capital gain results when a capital asset is sold at a price higher than the basis or original purchase price.

Capital gains can be long- or short-term. Short-term gains are on assets you’ve held for less than a year. They are taxed at the federal income tax rate.

Current Tax Rates (2026)

Long-term capital gains rates remain 0%, 15%, or 20%, depending on your taxable income and filing status (inflation-adjusted per IRS Revenue Procedure 2025-32)

Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

0% | $0 – $49,450 | $0 – $98,900 | $0 – $49,450 | $0 – $66,200 |

15% | $49,451 – $545,500 | $98,901 – $613,700 | $49,451 – $306,850 | $66,201 – $579,600 |

20% | Over $545,500 | Over $613,700 | Over $306,850 | Over $579,600 |

While most of your sale profit will be Capital Gains, any portion labeled as "Ordinary Income" (like inventory or depreciation recapture) may still qualify for the 20% QBI deduction, depending on the taxpayer’s circumstances and the nature of the income. [7]

Determining capital gains and the tax consequences takes the following process:

- Compute your basis, which equals the purchase price and any commissions or fees you paid.

- Calculate your realized amount, which is the sale price minus any commissions or fees paid.

- Subtract the basis from the realized amount to find the capital gain or loss.

- Determine tax by multiplying a capital gain by the correct tax rate. If there is a capital loss, you can use the loss to offset any gains and reduce the tax basis burden.

Key Considerations & "Tax Traps"

1. Installment Sales & Retained Earnings:

Capital gains affect other factors during the sale of an S corp, including installment sales. If you receive at least one payment for the sale of the S corporation's assets in future years, you can pay the capital gains tax over an extended period. Any undrawn profits or retained earnings will potentially help reduce the capital gains tax.

2. Ordinary Income Assets:

Not all profits will be taxed at the capital gains rate during the sale of an S corp. This only applies to capital gain income. You will be charged ordinary income tax rates on items such as inventory, accounts receivable, and property owned for a year or less.

3. Built-in Capital Gains (BIG) Tax:

You may experience double taxation via the built-in capital gains (BIG) tax if your company was ever solely a C corporation. Essentially, if you used a c corp formation service to establish your business and later elected S corporation status, any property obtained before the S corp election may be taxed twice if sold within the 5-year recognition period.

Shareholder Payments

During an S corp asset sale, the corporation liquidates and distributes sale proceeds to the S corp shareholders. For tax purposes, shareholder payments are generally made under employment consulting and noncompetition agreements to avoid double taxation.

Because an S corp is a pass-through entity, any gain by the company flows through and is paid by the individual shareholders on their tax returns. The payments will be taxed only once at the shareholder level. However, those payments will also be considered taxable at ordinary income tax rates for the shareholder taxpayers.

Note that employment and consulting payments will also be subject to employment taxes.

Net Investment Income Tax (NIIT)

The Net Investment Income Tax (NIIT) is a 3.8% tax imposed on individuals, estates, and trusts with high levels of investment income. This tax must be paid when income exceeds the statutory threshold amounts during an S corp asset or stock sale.

According to the IRS, NIIT thresholds are

- $250,000 for individuals who are married and filing jointly

- $125,000 for those who are married and filing separately

- $200,000 for single individuals.[8]

The most important legal distinction in 2026 is between Active and Passive shareholders.

- Active Shareholders: If you're an active owner (you materially participate in the business, like working 500+ hours a year or meeting other IRS tests), most gains from the sale of active business assets are not subject to the 3.8% NIIT.

- However, some parts of the sale, like depreciation recapture (tax on prior deductions) or gains from inventory, can still count as ordinary income and may trigger the NIIT if they don't qualify as active business income

- Passive Shareholders: Passive shareholders (no material participation) generally pay the 3.8% NIIT on applicable sale proceeds if the sale proceeds exceed thresholds.

Conclusion:

Maximizing your S Corp sale requires balancing valuation, structure, and tax strategy. The paperwork of a sale is intense, but you don't have to handle the transition alone. Ready to transition?

Let Swyft Filings handle the paperwork, from dissolution to new entity formation, ensuring your next venture starts on a solid legal foundation while you focus on your wealth.

Bibliography

- IRS. “Shareholder’s Instructions for Schedule K-1.” Accessed March 10. 2026

- IRS. “About Schedule D (Form 1040), Capital Gains and Losses.” Accessed March 10. 2026

- IRS. Form 8023. Accessed March 10. 2026

- IRS. Instructions for Form 8023. Accessed March 10. 2026

- IRS. “Topic No. 705, Installment Sales.” Accessed March 10. 2026

- SBA.gov. “7 Tax Strategies to Consider When Selling a Business.” Accessed March 10. 2026

- IRS. IRS releases tax inflation adjustments for tax year 2026. Accessed March 10. 2026

- IRS. “Questions and Answers on the Net Investment Income Tax.” Accessed March 10. 2026